The US and EU PMI manufacturing reports are going to take on greater importance, due to the fact that both economies are starting to weaken as COVID-19 dampen manufacturing activity.

German and French PMI data will also be watched extremely closely, as both economies manufacturing sectors are the engine of growth for much of Europe at the moment. A headline reading under 50 could sink the euro currency and EU stocks.

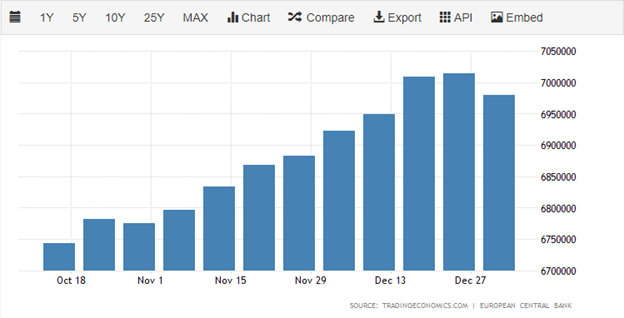

European Central Bank

Markets are not pricing in any chance that the ECB will be adjusting rates during this week meeting, however they will be looking for updates on the new policy measures the central bank recently introduced and the situation with EU inflation.

ECB policy members have also started to comment of the strength of the euro currency, which leaves plenty of room for ECB President Christine Lagarde to comment on the single currency during the press conference.

{kind=link}