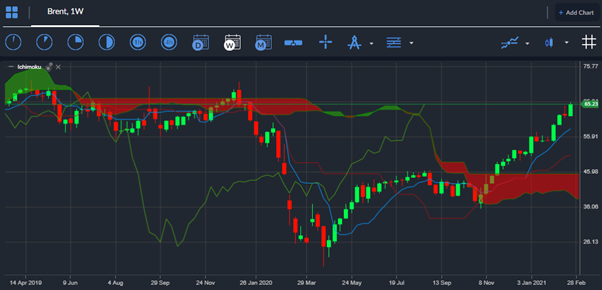

Bitcoin is trading lower by around -10 percent on the week. No major catalyst behind the sell-off, however, the crypto exchange Kraken observed major technical problems yesterday, with some big name cryptos dropping by as much as fifty percent.

Data Watch

During the European session, the release of UK jobs data and eurozone CPI is set to headline the economic docket. The EU CPI release is largely set to be a non-event; however, UK jobs data could be a big market mover for sterling and the FTSE 100.

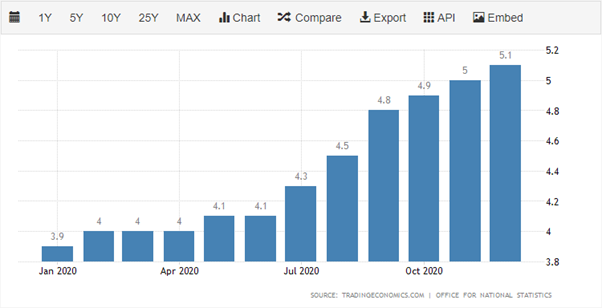

The UK unemployment rate is set to increase to 5.1 percent, while UK jobless claims are predicted to increase by 35,000. Average wages are forecasted to come in slightly higher. Overall, sterling has plenty of scope to correct lower on worse-than-expected jobs data as it trades at multi-year highs, around the 1.4100 level.

{kind=link}