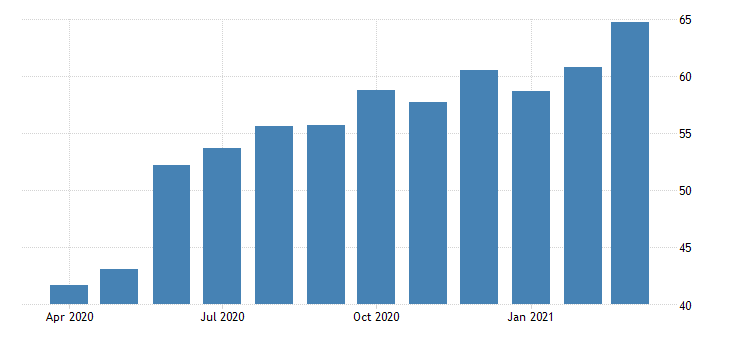

The major catalyst seems to have been good manufacturing data from the Institute for Supply Management (ISM) who survey more than 300 manufacturing firms to gauge the level of manufacturing activity. A reading above 50 is expansionary so a big jump to 64.7 in March from 60.8 the previous month, beat expectations by a long way. Factory activity was also higher in the IHS Markit Manufacturing PMI which has now risen to 59.1 in March showing that factory growth nearly at its highest activity on record. An increase in factory orders is a very bullish sign of economic growth but on the downside the increasing inflationary pressures are adding to costs that firms will need to pass on to consumers soon or risk feeling the negative deflationary effects to their bottom line.

Yesterday we had the weekly initial jobless claims which unfortunately rose above the 700k level again but to put a positive spin on it, the 4-week average was moving down and that is a good thing. Going into today’s jobs number the biggest guesstimate from those surveyed is for 1.1m jobs to be created as the US economy is opening up the retail and services sector more, with the consensus that we should see an increase on last month to around 640k. Because of the bank holiday weekend, the markets are either closed or running on reduced hours, so a big disappointing number or, fingers crossed a big expansion in the NFP number, will be greeted by very thin markets and we could see some volatility across any market that is trading. Best thing for retail traders would be to sit out and join in on a trend next week when the markets are back to full capacity after the holiday period.

{kind=link}