Midday Brief

Market sentiment in the broader financial markets is currently mixed going into the United States trading session as European stock markets trade in negative territory, while US stocks look to set to open in the green once again.

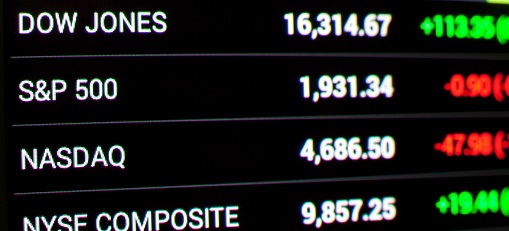

The Dow, Nasdaq, and S&P 500 also posted huge gains on Thursday as President Biden confirmed outside the Oval Office to reporters that US senators were working together on a bipartisan agreement for a massive $1.2 trillion spending bill.

Naturally, blue-chip stocks in the Dow exploded, while even industrial and material stocks on the S&P 500 added to their already strong weekly gain. As Wall Street opens it is apparent that investors liked what they saw and believe that the House and Senate are close to getting the massive spending bill across the line.

{kind=link}