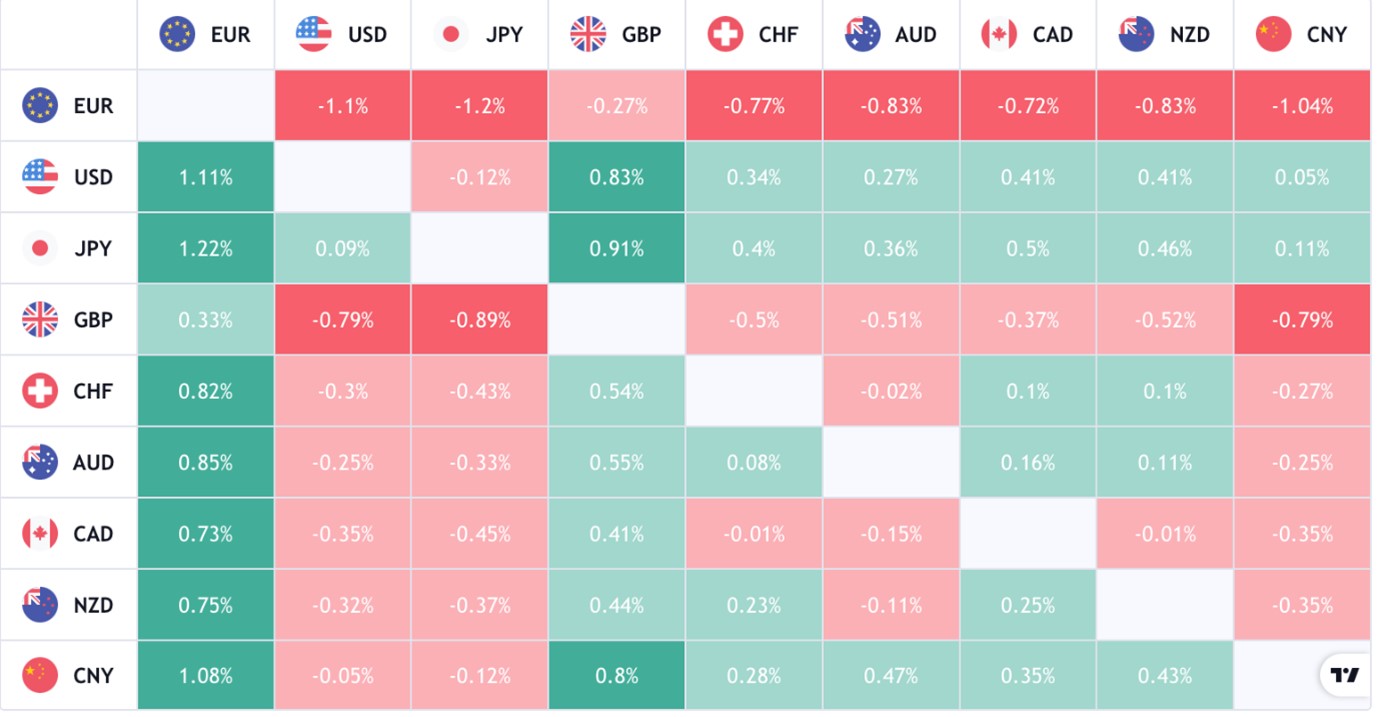

The forex heatmap shows that the euro and pound are getting hammered whilst the yen and US dollar are seeing most of the flows. Commodity prices are going a lot higher, but the currency pairs associated due to being crossed with USD are mixed.

German inflation data out today shows an acceleration to 5.1% annually for the month of February. This is largely in line with expectations and may add pressure on the ECB to act sooner with regards to rate hikes. That being said, ECB members are also going to consider not ending the asset purchase programme while the Ukraine situation creates this much uncertainty for the markets.

{kind=link}