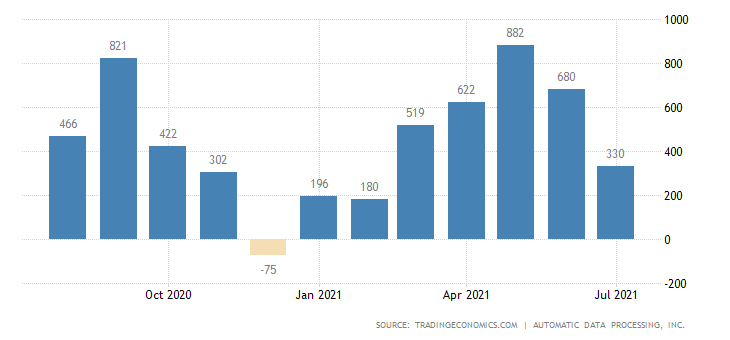

The ADP national employment report showed the number of jobs in the US private sector rose by 330,000 in July, coming in almost half of what was expected and really disappointing the markets.

Commenting on the data, ADP chief economist Nela Richardson said that “the labour market recovery continues to exhibit uneven progress, but progress nonetheless.” Richardson added that “bottlenecks in hiring continue to hold back stronger gains, particularly in light of new COVID-19 concerns tied to viral variants.”

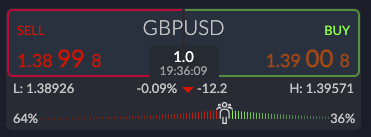

Fed Clarida who has a vote within the FOMC said today after the ADP number that he can certainly see the Fed announcing tapering later this year and would support announcing a moderation in asset purchases in 2021. He then went on to parrot Fed Chair Powell saying the economy has made progress toward goals since setting a substantial further progress bar for tapering of asset purchases. His personal view is core inflation hits 3% this year, and that he would consider it much more than a moderate overshoot of the Fed’s goal.

{kind=link}