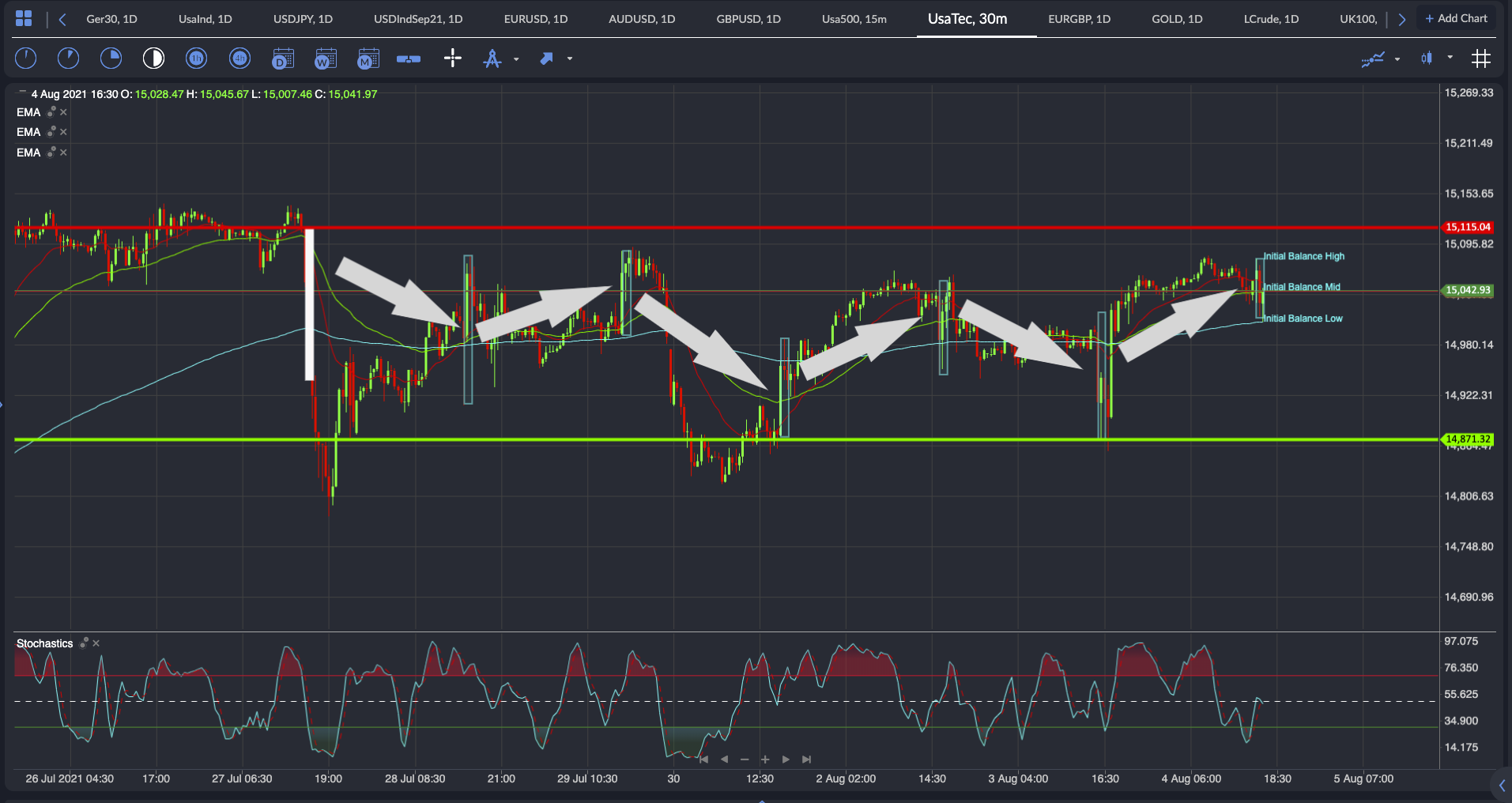

The question is how you know when the markets have switched from being momentum driven and trending to mean reverting and ranging?

The best way that I have found is to use the Initial Balance as my guide and see where it is with regards to the previous day. Today’s IB formed after the ADP figure and the US Markit/ISM PMI data. It also encompasses Fed Clarida’s speech which means there is little more news today that may affect the Nasdaq or S&P500, so with that in mind, if we haven’t been able to breakout of the IB with all that data, there is little probability that today is a trending day.

To further help you decide on whether to buy a breakout or sell a breakdown of the IB rather than fade it back to the midline, plenty of traders and investors have done statistical analysis on the probabilities of a trending move following on from a breakout of the IB.

As an example, over a period of 2,823 trading days, 95.36% of the time the IB High or IB Low was broken during the regular trading hours (RTH). The RTH is the US session. There was a 60% of the breakout reaching 50% of the IB range above or below the breakout line, within the days RTH. With 30% of those breakouts making a measured move higher or lower during the RTH.

If you were to conduct your own analysis on the last years’ worth of trading, you may find that these stats still remain relevant, and I certainly used the notion that if I were to trade the breakout that I aimed for at least 50% of the IB range and didn’t put too much expectancy on getting a measured move.

{kind=link}