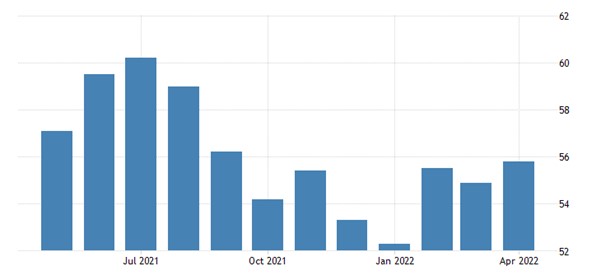

According to the S&P Global report released this morning, the Eurozone’s Purchasing Manager’s Index (PMI) Composite Output Index, which measures the performance made by service and manufacturing sectors jointly, rose in April from March, reaching 55.8 from 54, its seven-month high.

In the euro area, the Services PMI Activity Index also saw a monthly increase, going up to its 8-month high of 57.7. Manufacturing underperformed, as the Output Index fell to its 22-month low of 50.4, and the Manufacturing PMI fell to its 15-month low of 55.3.

{kind=link}