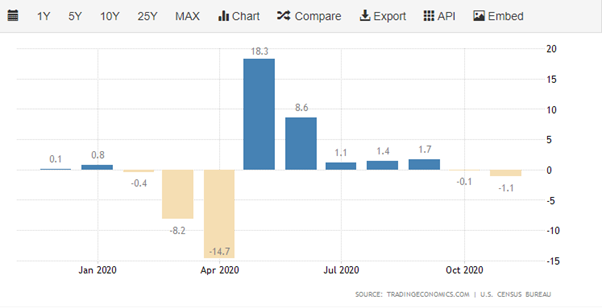

US retail sales are going to be the big focus during the US trading session, especially after FED Chair Powell’s speech and yesterday’s soft weekly jobless claims figures from the US economy, which moved close to 1 million mark.

Market expectations are for retail sales to have declined for a third straight month in the United States last month. Spending in bars and restaurants are expected to have plunged due to COVID-19 restrictions, while auto and gasoline components of the report are predicted to have rose.

It is difficult to know how the market will react, but I suspect that traders could move into the US dollar and sell stocks if retail sales come in worse-than-expected. Market sentiment is quite fragile today due to the risks hanging over the market, such as political uncertainty and rising COVID-19 infections globally.

{kind=link}