Bitcoin has recovered back above the $30,000 level after briefly dropping below the $29,000 level this morning. Cryptos have started to sell-off over recent days, following bearish comments surrounding Bitcoin and cryptocurrencies from US Treasury Secretary Janet Yellen.

Day Ahead

The European and US sessions are going to be heavily focused on PMI manufacturing data. The eurozone PMI is expected to come in better than last month, leaving plenty of scope for disappointment, and potential reason to sell the euro if the data prints a big miss.

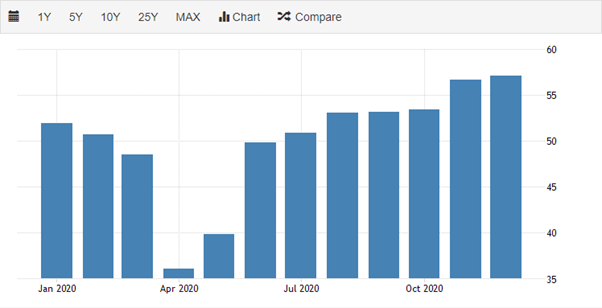

Sterling is notably weaker today and has fallen back under the 1.3700 level. The UK manufacturing PMI is expected to come in at 57.5, which would mark a multi-month high.

The US PMI manufacturing reading is set to be a big market mover, especially the prices paid component inside the PMI report. The release should set the tone for the US dollar index, stocks, and bonds for the next few days.