During the upcoming trading week, the Reserve Bank of New Zealand interest rate decision and a key testimony from Federal Reserve Chair Jerome before US Congress headlines the economic calendar. A host of Federal Reserve members are set to deliver speeches this week and comment on the current US economic outlook.

Aside from the two main events market participants will be looking forward to the release of GDP and IFO data from Germany, and raft of jobs numbers from the United Kingdom economy. Data from the United State is also heavily in focus this week as the world’s largest economy releases GDP, Jobs, Consumer Confidence, Housing, Spending, and Inflation numbers.

In terms of market themes, rising bond yields in the US and globally is likely to be a key feature this week. Stocks and gold are looking particularly sensitive to the dynamic and may continue to take a hit if bond yields remain on the rise.

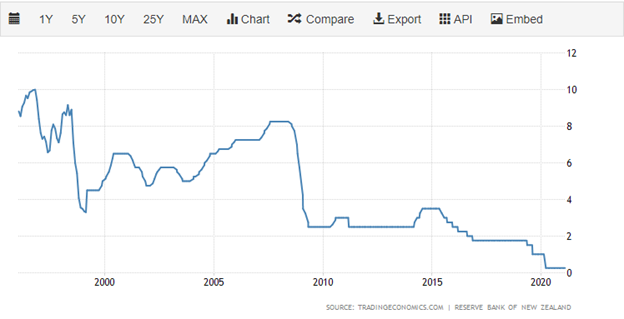

Reserve Bank of New Zealand

The Reserve Bank of New Zealand are widely tipped to keep interest rates on-hold this week, and sound slightly more hawkish than previous meetings. No change is expected in terms of bond purchases from the RBNZ.

RBNZ Governor Orr is expected to lay out the challenges that New Zealand economy still faces, despite the nation largely keeping COVID-19 under wraps during the pandemic. Recent economic data from New Zealand has painted a solid picture during the first quarter.

{kind=link}