As the market action in Europe starts to warm-up the main theme today in financial markets has been rising commodity prices. Iron ore and copper prices in particular are up big already on Monday, as risk sentiment and the ongoing reflation trade gathers pace.

Commodity-related currencies such as the Australian dollar, New Zealand dollar, and Canadian dollar are the strongest gainers in the foreign exchange market on Monday, while safe-haven currencies, like the Japanese yen and Swiss franc, are down on the day.

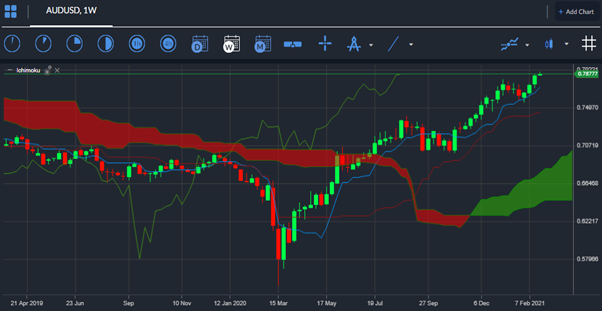

The Australian dollar is typically the main beneficiary when iron ore prices are moving higher, and this has been the case the morning as the AUDUSD pair has risen to a new multi-year high, of 0.7906.

{kind=link}