During the upcoming trading week global central banks and consumer price inflation releases are set to dominate the economic docket. The main event of the week will be the US CPI release, however, central bank decisions from the Bank of Japan, Bank of Canada will also be very important for currency and stock traders.

Other key macroeconomic releases to watch out for this week to watch include FED Chair Powell’s testimony before US Congress, United Kingdom Consumer Price Index numbers, and the Reserve Bank of New Zealand interest rate decision and policy statement.

This week will also see the release of harmonized CPI inflation numbers from the German and Australian economies, United Kingdom jobs data, and the monthly jobs report from the Australian economy.

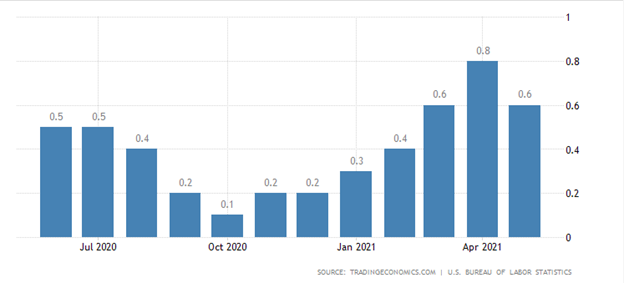

US Consumer Price Index

The highlight on the economic docket this week is without a doubt going to be the US CPI release, following the release of some of the strongest inflation numbers the country has seen in over decade during the last fiscal quarter.

Some market participants have noted that the FED’s worst case scenario would be a low growth and high inflation environment, and I tend to agree with this assessment. This month’s CPI increase is expected in at 0.4 percent, which is not as high as last month and means CPI is trending lower for a second consecutive month.

Last month’s Consumer Price Index increased by 0.6 percent on a seasonally adjusted basis after rising 0.8 percent in April. The index for used cars and trucks continued to rise sharply, increasing 7.3 percent in May and accounting for about one-third of the seasonally adjusted all items increase.

The food index increased 0.4 percent in May, the same increase as in April. The energy index was unchanged in May, with a decline in the gasoline index again offsetting increases in the electricity and natural gas index.

{kind=link}