Copper prices have come down slightly after yesterday’s four percent pump higher over fears about copper supply in Chile. Rising South American COVID-19 infections is also affecting the price of crude oil today.

Bitcoin is under slight pressure on the cryptocurrency market as the pioneer crypto fails to crack the $60,000 level. Bitcoin’s market dominance has been declining over recent days as other altcoins, such as Ripple, and Ethereum, continue to significantly outpace Bitcoin in terms of gains.

Data Watch

The economic calendar in the European session is fairly busy today, with Swiss National Bank total deposit data coming out, and the release of the eurozone official unemployment rate. The Sentix investor confidence survey from the eurozone is also set for release this morning.

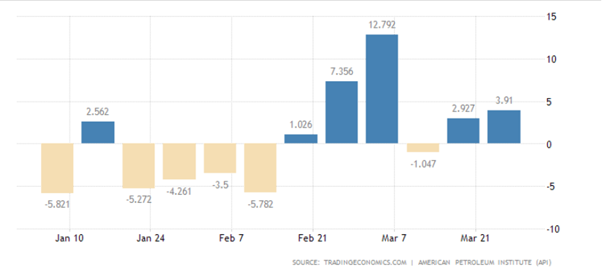

During the United States trading session the release of JOLTS job openings will be closely watched after last Friday’s blockbuster jobs number. Oil traders also look to the API weekly crude inventory release.

{kind=link}