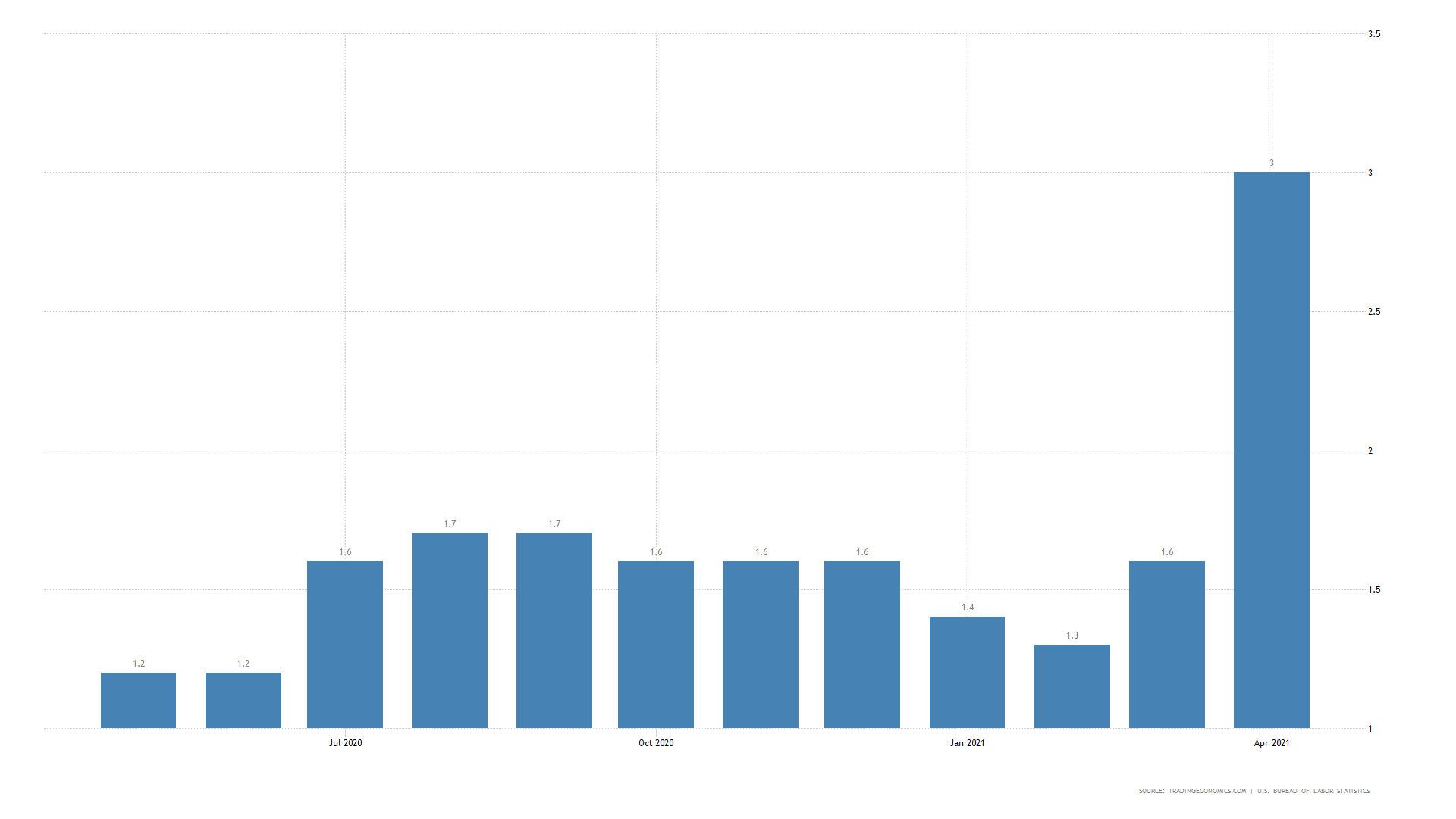

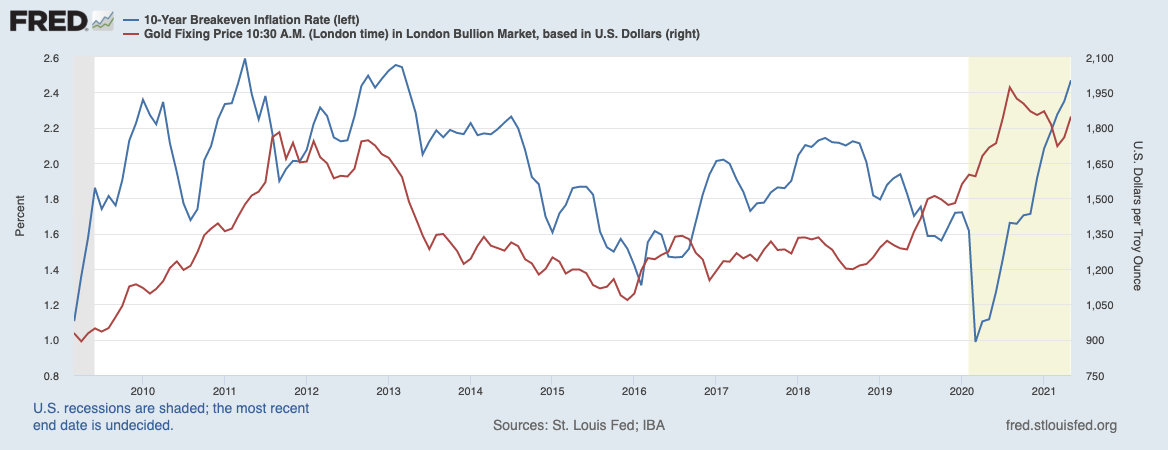

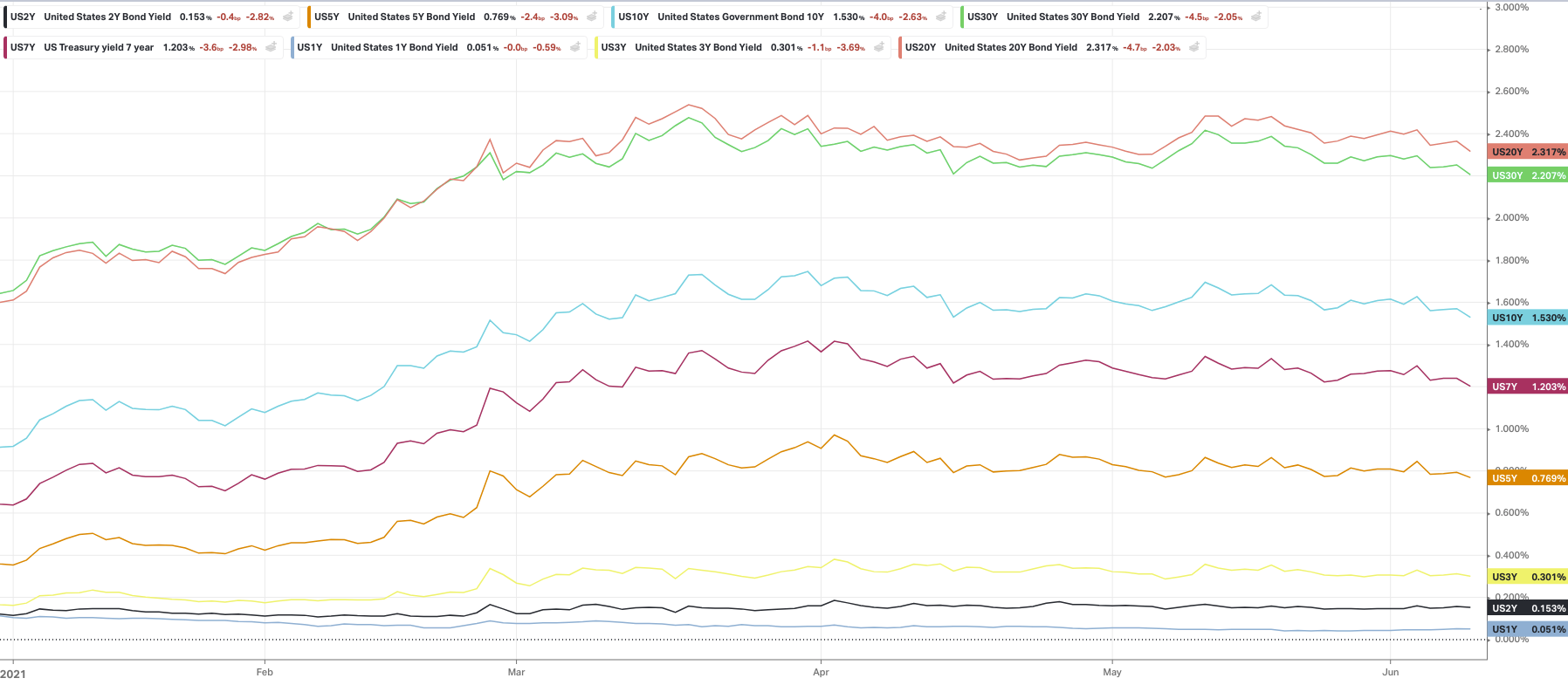

US10 year yields remain higher year on year due to continued uncertainty over the economic recovery and inflation. Moreover, real rates dropped as inflation expectations, as signalled by TIPS breakeven, increased. Fears over inflation, and whether it will be transitory or not, continue to be supportive for gold. Should higher levels of inflation become established, gold’s appeal as a hedge against a reduction in purchasing power would be improved.

Another thing that is a bit of an unknown is the effects the new Basel 111 laws will have on the derivatives gold markets. Gold is classes as a Tier 1 asset and banks need to hold this level of asset on reserve to maintain their supplementary leverage ratios in the USA. But at the end of June the European commercial banks will have to be compliant with new legislation. Which in itself could be the end of the non-allocated/ non-physical markets in precious metals. Which could potentially give the physical metal a boost in price as demand outstrips supply.

The Basel 3 accord is a set of global financial reforms developed by the Basel Committee on Banking Supervision under the domain of the Bank for International Settlements (BIS), an organization headquartered in Basel, Switzerland. These coming changes in bank system operations are to strengthen regulation, supervision and risk management within the worldwide banking industry.

The goal of the forthcoming Basel regulations is to limit the levels of risk that banks take on in the pursuit of profits, which would hopefully prevent a major worldwide financial crisis if markets turn negative.

The London Bullion Market Association trades an average of $20 billion in gold every day, which is more than $5 trillion annually. Virtually all of this trading is in the form of unallocated precious metals, so any signs of stress should be seen here first.

{kind=link}