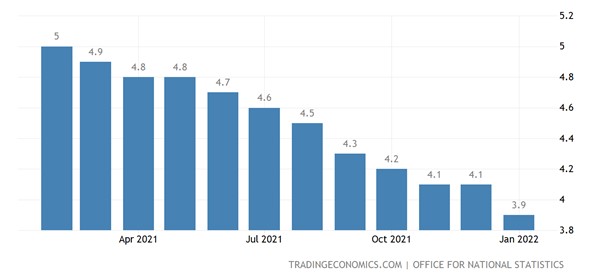

According to a report published by the Office for National Statistics this morning, the United Kingdom’s unemployment rate dropped by 0.2 percentage points in January to 3.9%, bringing it back to its pre-pandemic level. During the same period, the employment rate improved by 0.1% to 75.6%, according to the report, remaining one point below the pre-crisis figure. While total working hours increased, they remained lower than in February 2020.

{kind=link}