Market Wrap

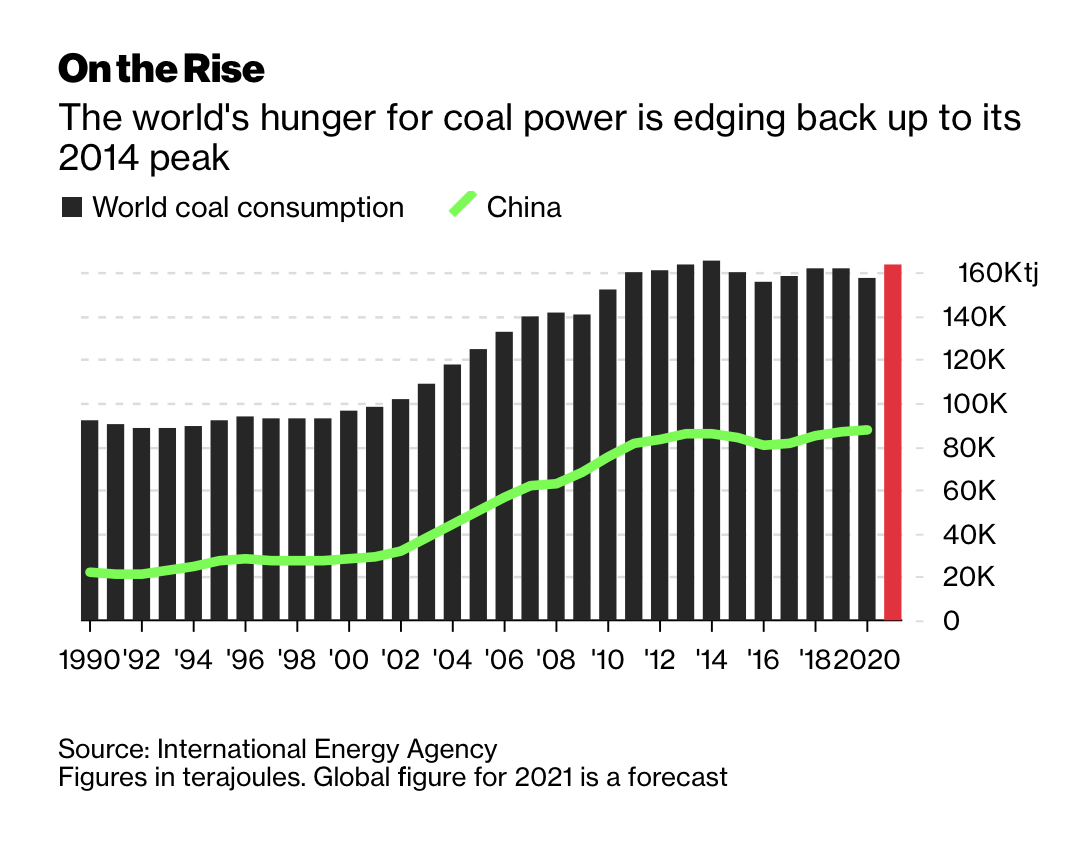

After a week-long holiday in China, iron ore prices rose on Friday with market participants optimistic about demand prospects for the raw material in the world’s top steel producer.

Due to China’s electricity shortage, electric arc furnaces that use iron scraps to produce steel are at risk of being shut down, which means blast furnaces that use iron ore must produce more steel.

The most-traded January iron ore was 4.9% higher $118.24 a tonne Friday morning rising to $122 today, its strongest since September 6.

{kind=link}