Employment data out today showed US Initial Jobless Claims fell as Americans filing new claims for unemployment benefits dropped to 376k, which is the lowest level in over a year.

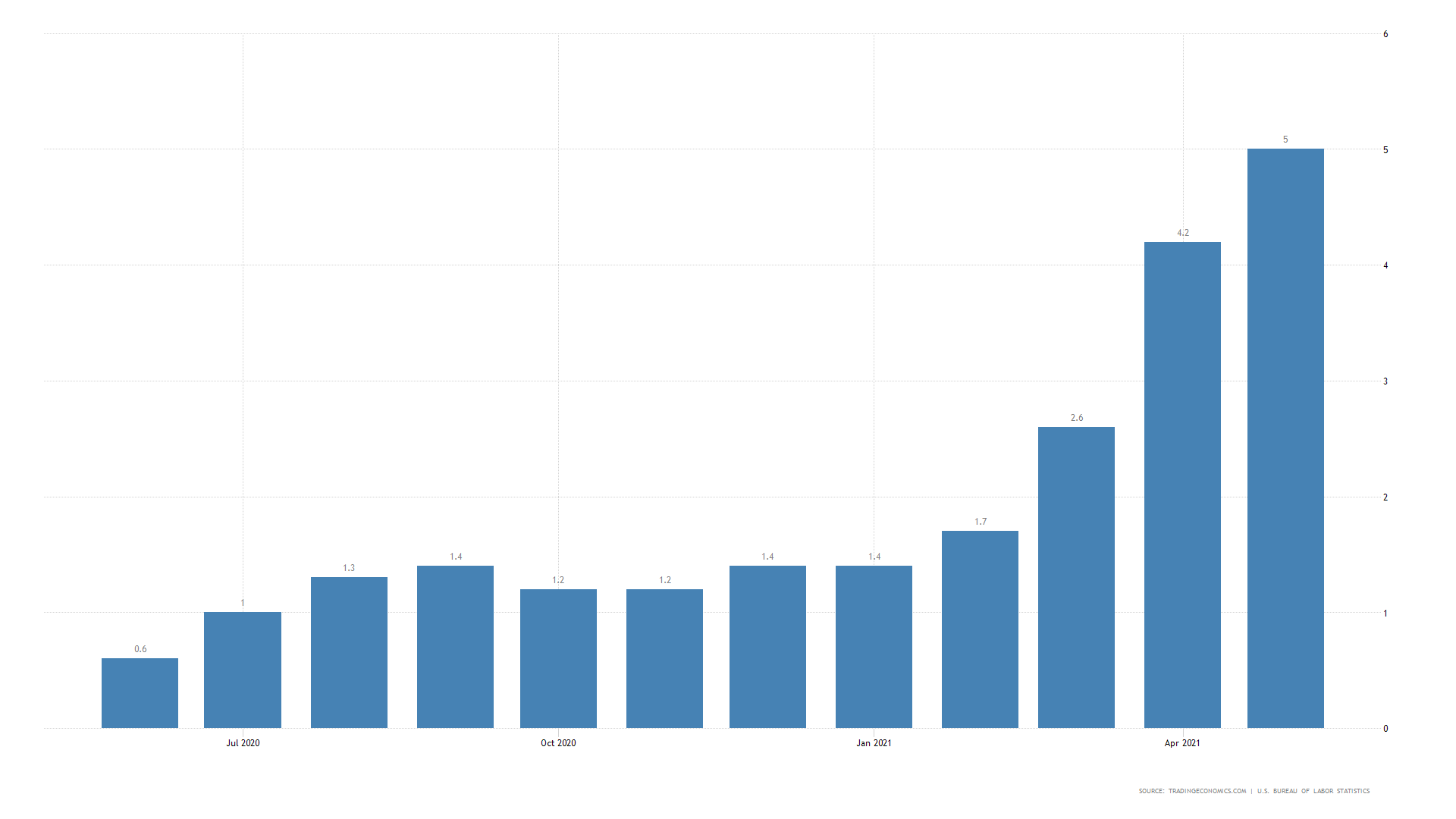

The US dollar is still unfortunately pinned to the $90, which is not good news for anyone trying to capture a trending move on one of the major crosses. It looks like the only way to get the US dollar off this level if the Fed actually make noises towards adjusting policy. Which they could do if employment data stays robust and inflation now sticks above 2% in the CPI and PCE readings.

{kind=link}