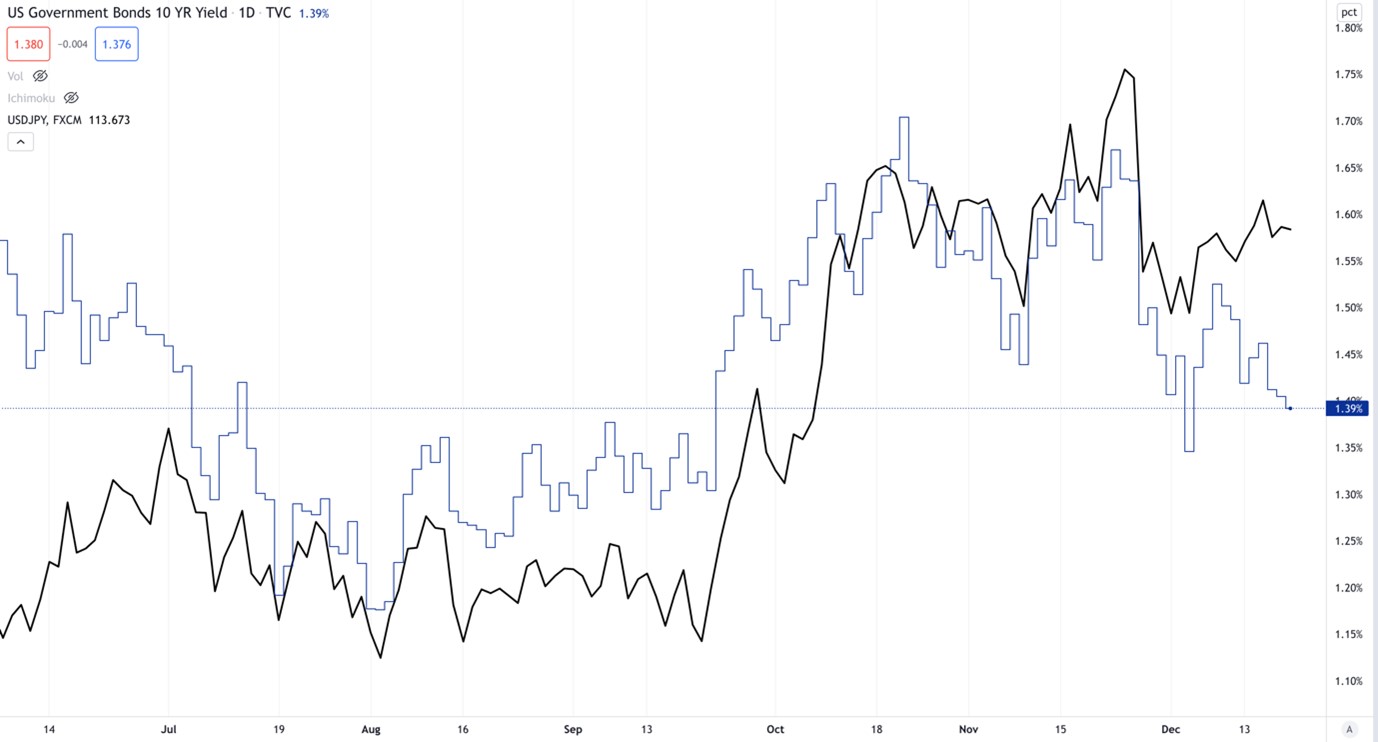

There has been an appreciation in the US dollar versus the yen since the bottom of the COVID-19 pandemic, first as a safe haven alongside the yen, then as a reflation trade as the USA pushed everything behind the development of vaccines and the subsequent rollout to economic reopening. This led to the states reopening faster than Japan and the economy recovering quicker. Japan’s problems with vaccinations and lockdowns during the Olympics have been a huge drag on its economy and the yen has fallen.

The USD2trn Build Back Better bill proposed by Joe Biden has also contributed to the strength of the US dollar. This bill is now in trouble with Senator Joe Manchin withdrawing his support. On a promise from Biden that Manchin would support at least a $1.75trn Build Back Better bill, Progressives in the House voted for the $550bln infrastructure package earlier this year. According to the White House, Manchin’s move is an “inexplicable reversal”. The news of the failing Build Back Better bill has hurt US yields and the US dollar and has led to the greenback falling against the EUR, CHF, and JPY.

{kind=link}