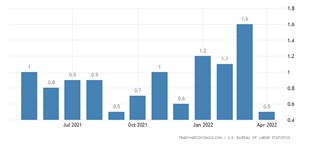

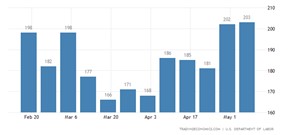

Today’s US economic data showed a big monthly drop in PPI, which shows that inflationary pressures on prices could be slowing, which is what the Fed need to happen. Fed Chair Powell’s press conference was all about how the Fed intends to stabiles prices and this is a big step towards doing that. Unfortunately for the Americans, more people are now having to claim unemployment benefits as not only did this week’s number come in higher than expectations, but there was also a higher revision for last weeks too.

{kind=link}