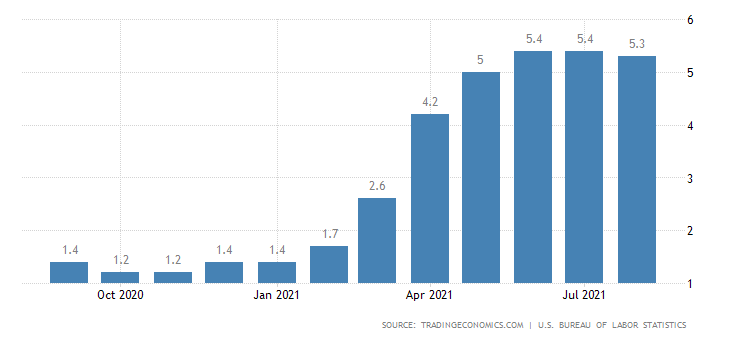

According to the US Bureau of Labour Statistics data, the Consumer Price Index (CPI) for all items in the country grew 5.3% year-on-year in August. Month-on-month the index was 0.3% higher. This month’s CPI came in under expectations and will cast doubt on the FOMC taper probabilities in the coming weeks.

Once again energy contributed the most to the monthly increase, rising 2.0%, mainly due to a 2.8% growth in gasoline prices. The index for food climbed 0.4%. These two parts to the inflation data are what US consumers are worried about as weekly shopping and living expenses are rapidly rising.

{kind=link}