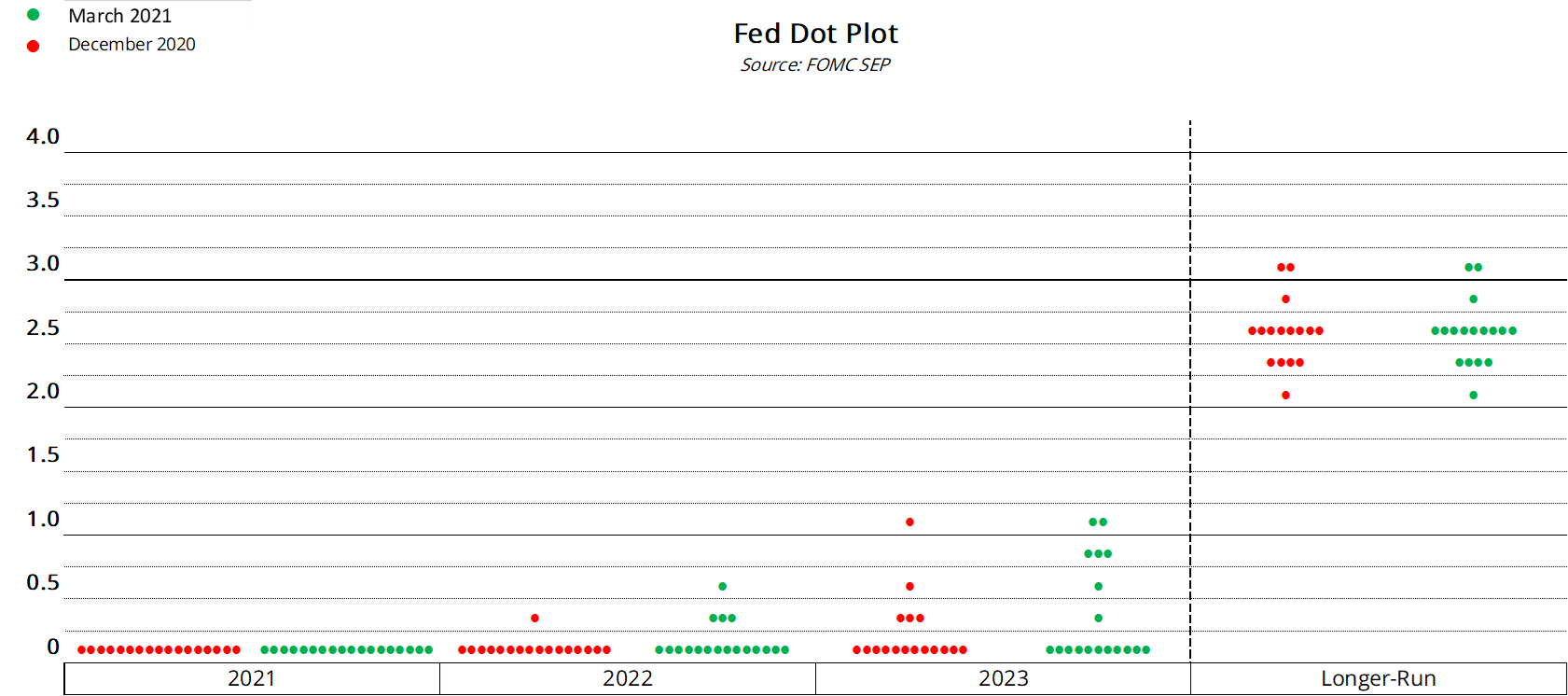

Judging by the FOMC rate decision the strong data is not imminent and if you go by their dot plot for rates, the stronger data is not likely to materialise before 2023. So, for the next 2 years, at least, the sovereign rate setter is keeping things unchanged. Which for some market participants will sound like folly, and it is they who will continue to sell US Treasuries in an attempt to push the yields higher, in an attempt to force the Fed to change course. The saying is “don’t fight the Fed”, so it will make for an interesting battle in the coming months.

The overall Fed themes are Dovish, so the expectations if you follow that line is, that the US dollar will weaken, inflationary pressures may arise, but the year-on-year data from March through April 2020 is about to fall out of that dataset, so the rise in recorded inflation will normalise again, having come from such a low base due to the economic shutdown.

{kind=link}