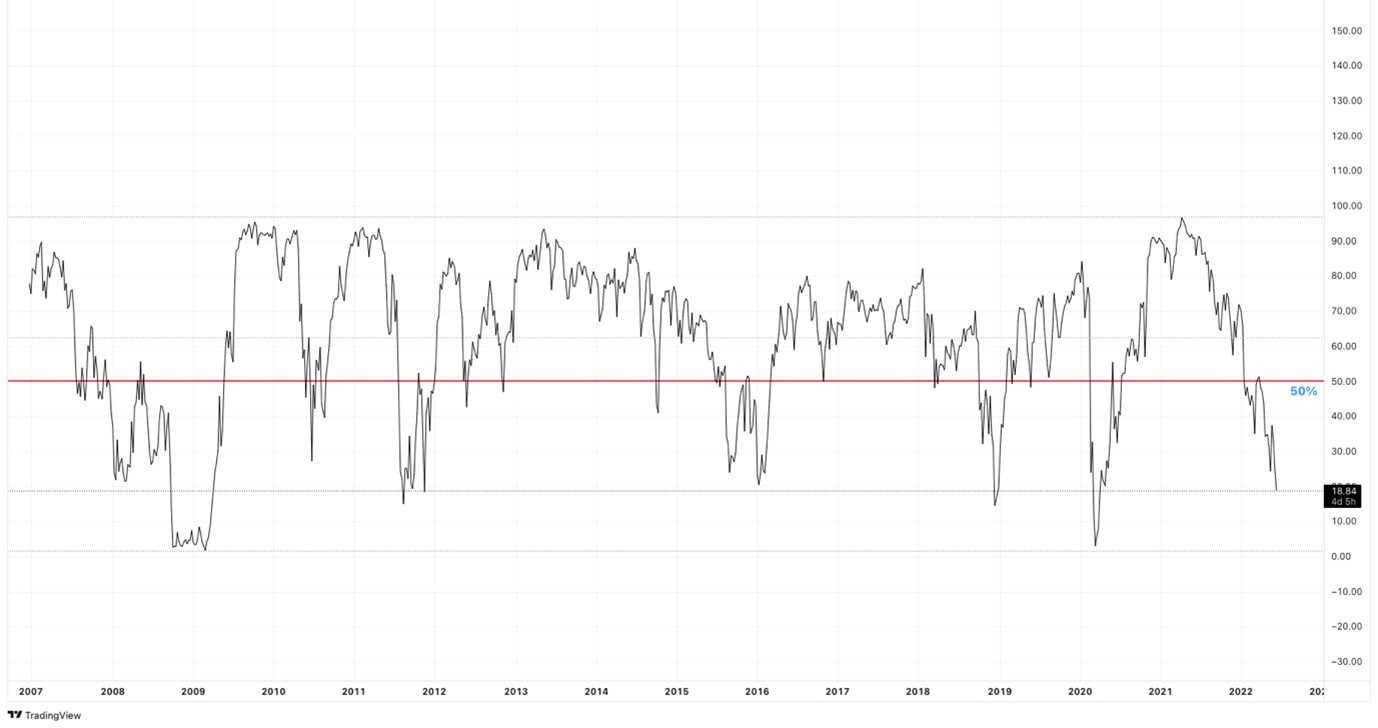

The S&P500 has dropped hard along with the other US major indices and within the index there are only around 19% of companies trading at or above their 200-day moving average. The Nasdaq has led the way lower with a near limit down day, and currently trading -4% (at the time of writing). Over the last week of trading activity, the Nasdaq is down -9.94%, with only the Italian bourse lower, coming in at -11.04% over the last 7 days. Gold has also plunged more than 2% and silver has lost as much as 4% amid this major sell-off.

There is a big US corporate tax payment due in this week which will be a liquidity drain on the markets. If it were not for the rising cost of energy and inflation, I would put todays moves down to uncertainty around the Fed but also at the need to find a liquid asset to sell, to pay the tax. If that had been the dominant fundamental driver, we would be expecting a higher close later in the week.

It now makes sense that the S&P500 reaches for the weekly 200-period EMA and for investors to get another chance to buy the index off the dynamic support. Though a close below and we could be in for a really wild ride lower.

{kind=link}