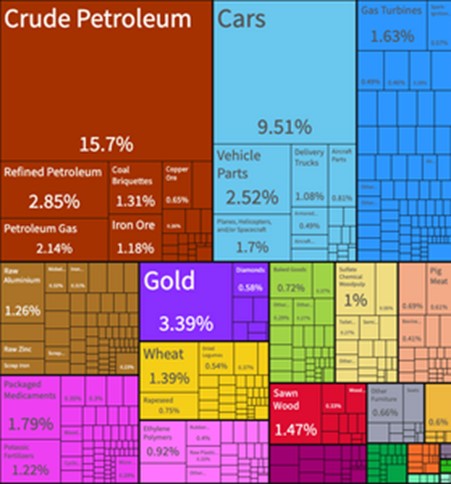

In the case of the USDCAD, a strong greenback can be used to import Canadian exports. According to The Observatory of Economic Complexity, Canada was the number 10 economy in 2019 and the number 11 world exporter. The top of Canadian exports is Crude Petroleum, with Cars, Gold and Refined Petroleum products mostly going to the United States.

A lot has happened in the last 2-years due to the pandemic not only shutting us all down but we’re also seeing the continuation of disruptions even after economies re-open. What can be assumed though is that the Canadian economy will be closely tied to the exports of Oil in the future.

With the third-largest oil reserves in the world, Canada is the world’s fifth-largest oil producer

4.6 million barrels per day of crude oil were produced by Canada in 2018; this makes the country a major source of safe, reliable crude oil for international markets. Furthermore, Canada holds one of the world’s largest oil reserves, surpassed only by Saudi Arabia and Venezuela. The country has 168 billion barrels of proven oil reserves, of which 164 billion barrels are oil sands. In 2018. 96% of Canadian crude oil exports went to the USA.

Canadian oil is different from that found in Texas or the Gulf of Mexico. A natural mixture of sand, clay or other minerals, water, and bitumen is referred to as oil sand. Two methods can be used to extract bitumen, depending on the depth of the deposits below the surface. But the key takeaway is that there is more processing needed with this oil sand, which means that it’s also more expensive to produce. Therefore, it is probably in the Canadian oil industries best interest to have the US dollar stronger than the Canadian dollar to give them the incentive to buy and to keep the margins reasonable for Canadian producers.

{kind=link}