Other highlights on the economic calendar include consumer price inflation and retail sales from the Canadian economy, and a raft of data points from the United States economy including weekly jobs, housing, and manufacturing numbers, which could affect the greenback.

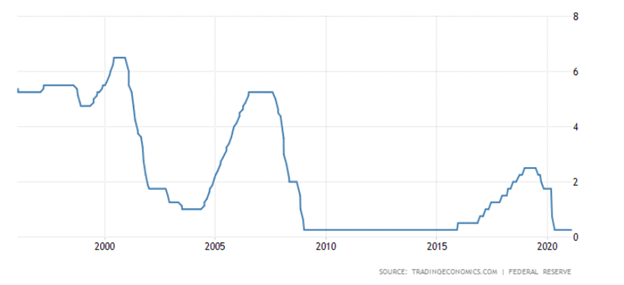

Federal Reserve

This week’s FOMC rate decision is likely to set the overall tone for financial markets, especially the central banks official policy statement to market participants. The economic projection from members of the Federal Reserve is probably going to be the most contentious part of this week’s meeting.

Assuming that the Federal Reserve leaves policy unchanged, the FED economic projections will give a key insight into whether members of the US central bank truly believe that the US economy is in recovery mode or. FED members will probably be careful and strike a fine balance between positivity and not sounding too optimistic.

{kind=link}