During the upcoming trading week, the Federal Open Market Committee policy meeting is set to headline the economic docket as traders await the FED’s latest thoughts on the United States economy, QE, and rates.

Other key macroeconomic and policy decisions this week include the release of eurozone PMI data for the month of September and important rate-setting decisions from the Bank of England, Bank of Japan and People’s Bank of China.

This week will also see the release of the RBA meeting minutes German IFO data, and a raft of Consumer Confidence data, and services PMI and Manufacturing data from the UK.

Traders will also be keeping a close watch on the Chinese Evergrande situation and the ongoing talks and discussions from the US debt ceiling. Both could have huge implications for global stocks and the US dollar.

Eurozone Preliminary Manufacturing PMI

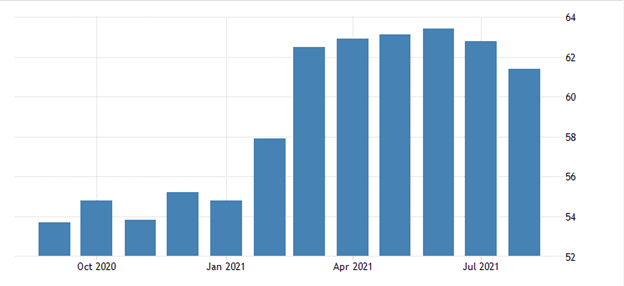

The eurozone Manufacturing PMI has been gradually trending lower over recent months, although the data has not fallen off a cliff just yet, which gives economists some hope that the decline will only be gradual.

Last month the EU PMI reading stood at 61.4 in August 2021, which was basically little changed from a preliminary estimate of 61.5 and below July’s final 62.8. The September reading is supposed to show a minor uptick to 62.0.

Some concern is still warranted given COVID-19 related issues and slowing Chinese growth. Manufacturing production growth eased to a six-month low last month, although total new orders increased for a fourteenth straight month and new export business also grew at a marked rate. This preliminary PMI release could be a big market mover for euro currency later this week.

{kind=link}