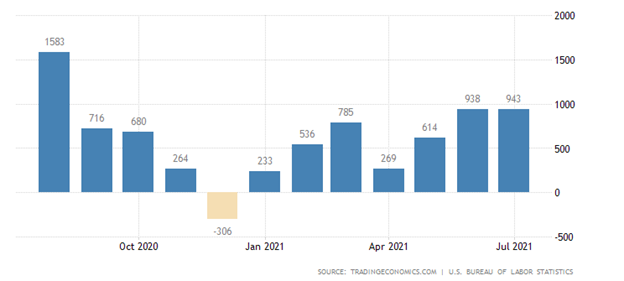

During the upcoming trading week, the release of the United States Non-farm payrolls job report is set to be the main focus for financial markets, following last month’s multi-month record-setting 900,000 plus headline number.

Other key highlights on the economic docket this week include the closely watched ISM manufacturing report, UK PMI services report, and key retail sales numbers from the eurozone economy.

This week we also see GDP data from the Swiss and Australian economy, plus traders and investors will be reacting to the outcome of the recent Jackson Hole Economic Symposium.

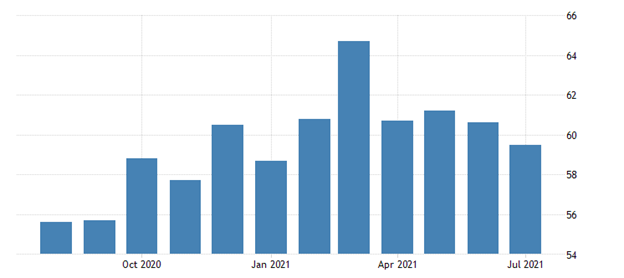

ISM Manufacturing Report

Analysts are expecting another weaker ISM manufacturing report for August, with a 59.1 number, providing further evidence that the US manufacturing sector is now starting to slow.

Last month the ISM Manufacturing PMI fell to 59.5 in July of 2021, marking the weakest ISM survey in 6 months, compared to 60.6 in June and below forecasts of 60.9. The reading pointed to the second consecutive month of slowing factory growth as new orders 64.9 vs 66 in June.

{kind=link}