During the upcoming trading week, the ongoing breakout in the US dollar index and the planned $1.9 trillion stimulus package from the Biden administration are set to take centre stage. The US dollar is gaining momentum in the foreign exchange market and is set to be a be theme for financial markets this month.

US stimulus is also coming back in the markets focus after the proposed $1.9 trillion stimulus package gained support in the House of Representatives this week. Market optimism is likely to remain at elevated levels due to the prospect of massive stimulus hitting the US economy.

In terms of the economic docket next week the release of US CPI inflation is set to be the main event, as market participants look for signs of inflation in the United States economy. UK quarterly and monthly Gross Domestic Product, US earnings season, and US sentiment data are other notable events on the economic calendar next week.

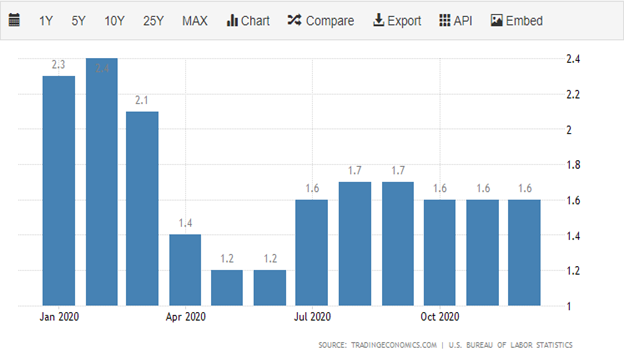

US CPI Inflation

Inflation in the American economy is a hot potato for financial markets at the moment. The Federal Reserve talked down the inflationary prospects for the US economy during the January policy meeting, however, the real economy is showing signs of ongoing price pressures.

This week’s Consumer Price Index could be a big market mover if the headline CPI number comes in hot. A better-than-expected CPI number also has the ability to accelerate the ongoing breakout in the greenback and create a perfect storm in the foreign exchange market and bond market.

{kind=link}