During the upcoming trading week, the economic calendar is heavily dominated by central banks, as we the release of meeting minutes from the FOMC and the Reserve Bank of Australia.

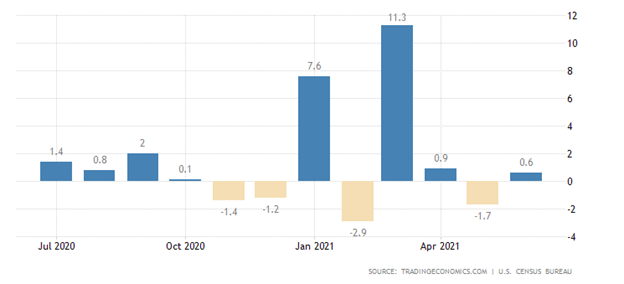

Other key highlights on the economic docket this week include the release of United States monthly retail sales and also Gross Domestic Product data from Japan and the eurozone economies.

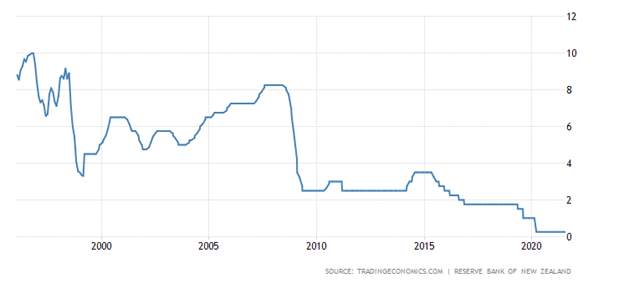

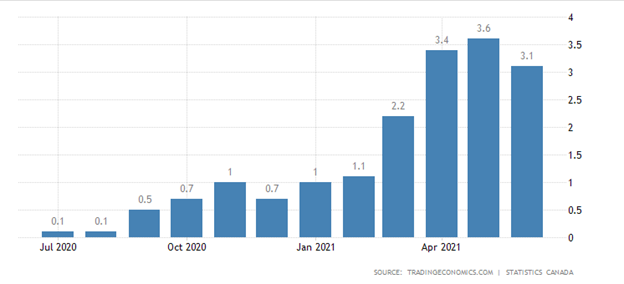

This week will also see the release of the Reserve Bank of New Zealand policy decision, and a raft of important data points from the Canadian economy, including retail sales and CPI inflation.

FOMC Minutes + US Retail Sales

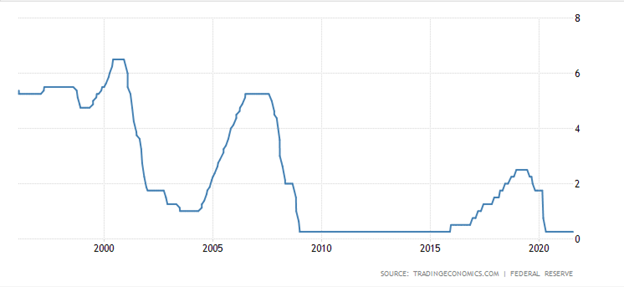

The undoubted highlight on the economic docket this week is the FOMC meeting minutes as taper talk starts to increase after the recent robust July employment report with showed that nearly one million jobs had been created.

At the last policy meeting the Fed left the target range for its federal funds rate unchanged at 0-0.25% and bond-buying at the current $120 billion monthly pace during the July 2021 meeting.

Traders will be waiting to see if the central bank will offer some hints that asset purchases could start being reduced soon in spite of the threat to growth from delta variant of the coronavirus.

{kind=link}