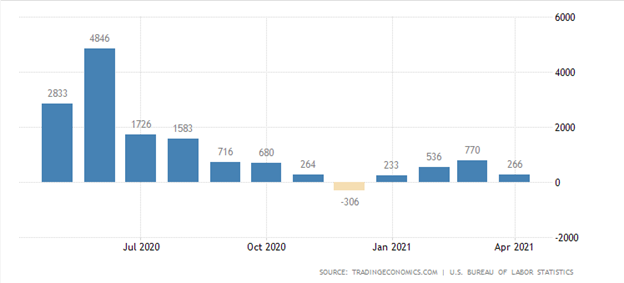

During the upcoming trading week, the release of the United States Non-farm payrolls job report is set to be the main focus for financial markets, following last month’s lacklustre headline number of 260,000.

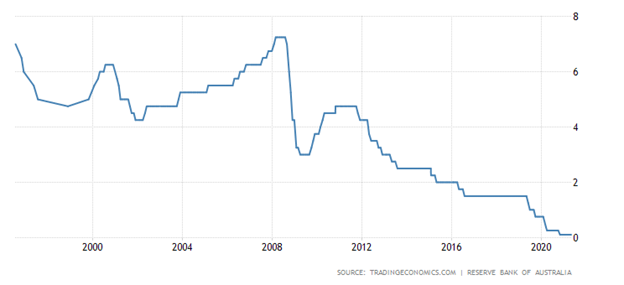

Other key highlights on the economic docket this week include the Reserve Bank of Australia interest rate decision and monetary policy statement, and the ISM manufacturing report from the United States.

This week will also see retail sales and CPI inflation numbers from Europe, monthly jobs and Gross Domestic data from the Canadian economy, and retail sales figures from the Australian economy.

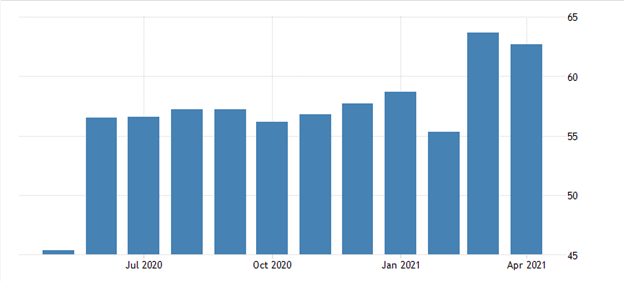

ISM Manufacturing Report

The ISM Non-Manufacturing PMI is expected to come in at 62.9 for the month of May, which would mean that manufacturing activity expected 0.2 more than the previous month.

Last month the ISM survey from the US dropped to 62.7 from an all-time high of 63.7 in the previous month, which was just below market expectations of 64.3, indicating slowing growth in the services sector.

The survey’s measure of prices paid by services industries rose to 76.8, which was in fact the highest reading since July 2008. Inflation will be closely scrutinized inside this report, and if we see more strong inflation then the greenback could surge against other currencies.

{kind=link}