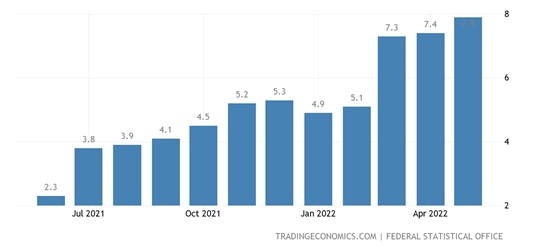

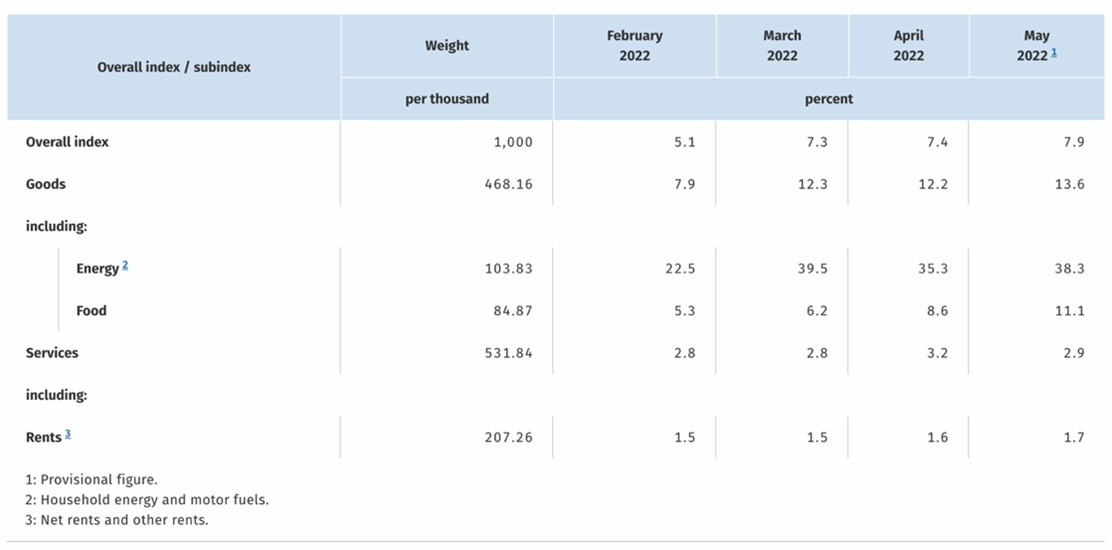

Fuel prices rose 38.3% year over year in May, while food prices increased 11.1%. Pandemic-related disruptions in supply chains were also noted in the Destatis report. The disruptions and uncertainty around the Ukraine invasion by Russia will keep inflation high especially if the European Union comes to an agreement today to ban Russian energy imports.

German Chancellor Olaf Scholz has been reported to have said today that there is “every indication” European Union member states will agree on sanctions on Russian oil as they meet for a summit today and tomorrow. “All that I hear is that there really are discussions that are being held with a will to reach an understanding”. “I am firmly convinced that today, tomorrow, we can debate further for a good solution,” he added, warning that “no one can predict” if an agreement will actually be reached. However, European Commission President Ursula von der Leyen said she does not expect a deal in the next 48 hours.

{kind=link}