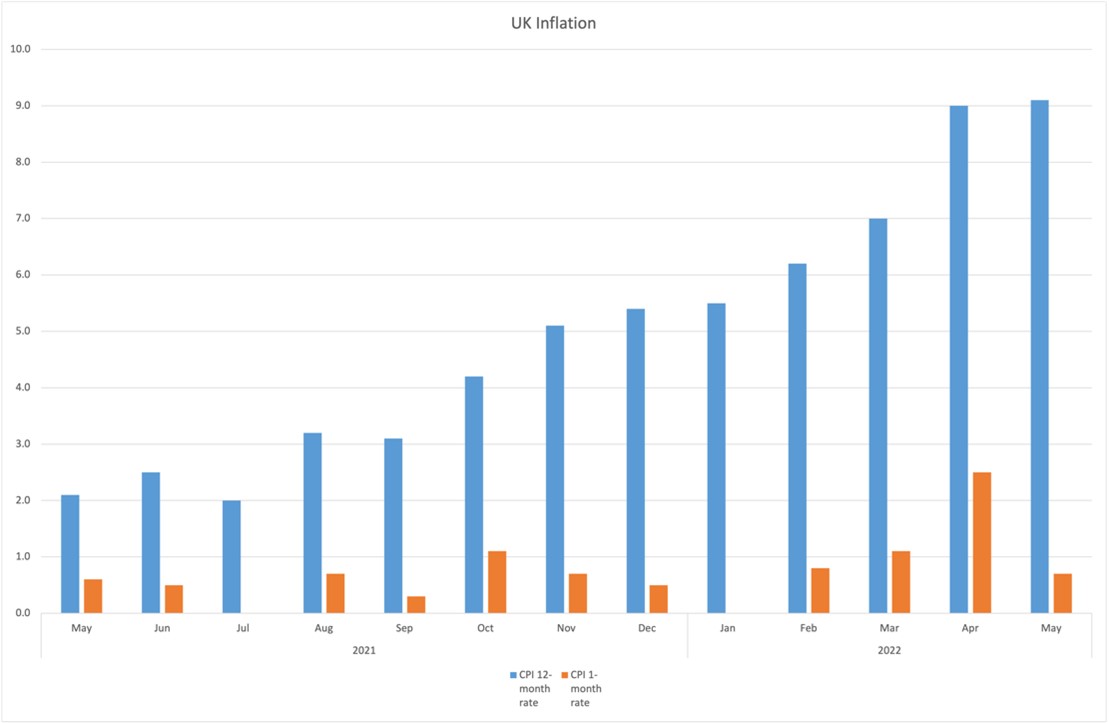

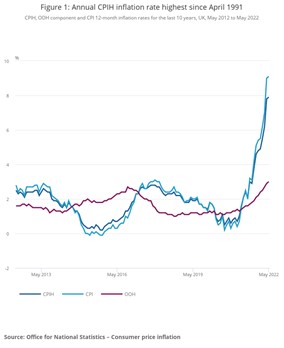

The Consumer Prices Index including owner occupiers’ housing costs (CPIH) rose by 7.9% in the 12 months to May 2022, up from 7.8% in April. The largest upward contributions to the annual CPIH inflation rate in May 2022 came from housing and household services (2.79 percentage points, principally from electricity, gas and other fuels, and owner occupiers’ housing costs) and transport (1.50 percentage points, principally from motor fuels and second-hand cars).

{kind=link}