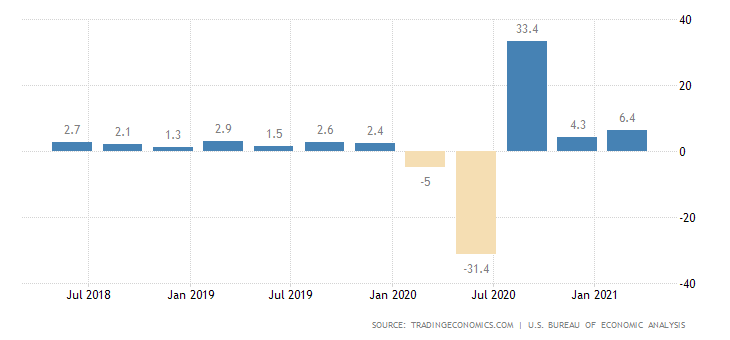

US GDP figures show the economy grew by an annualized 6.4% in the first quarter, matching the flash reading but under analysts’ expectations of a higher reading of 6.5%. US core PCE prices readings were higher than expected coming in at 2.5% for Q1 and tomorrow we get the PCE index that the Federal Reserve will be watching for their inflation modelling. The continuing jobless claims data that came out today will also be welcome news for the Fed as it shows the latest reading falling back down from the previous week. Along with the inflation and jobs data, the market is in wait and see mode for what the US senate can do to get President Bidens infrastructure bill through. Currently the Republicans are proposing a $928bln counteroffer, with the likelihood that the two side meet somewhere between that and the $1.7trn figure outlined earlier.

Tomorrow is a big day in the markets as it will be the end of month session before an extended bank holiday weekend.