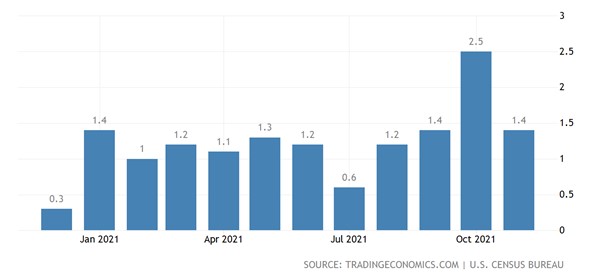

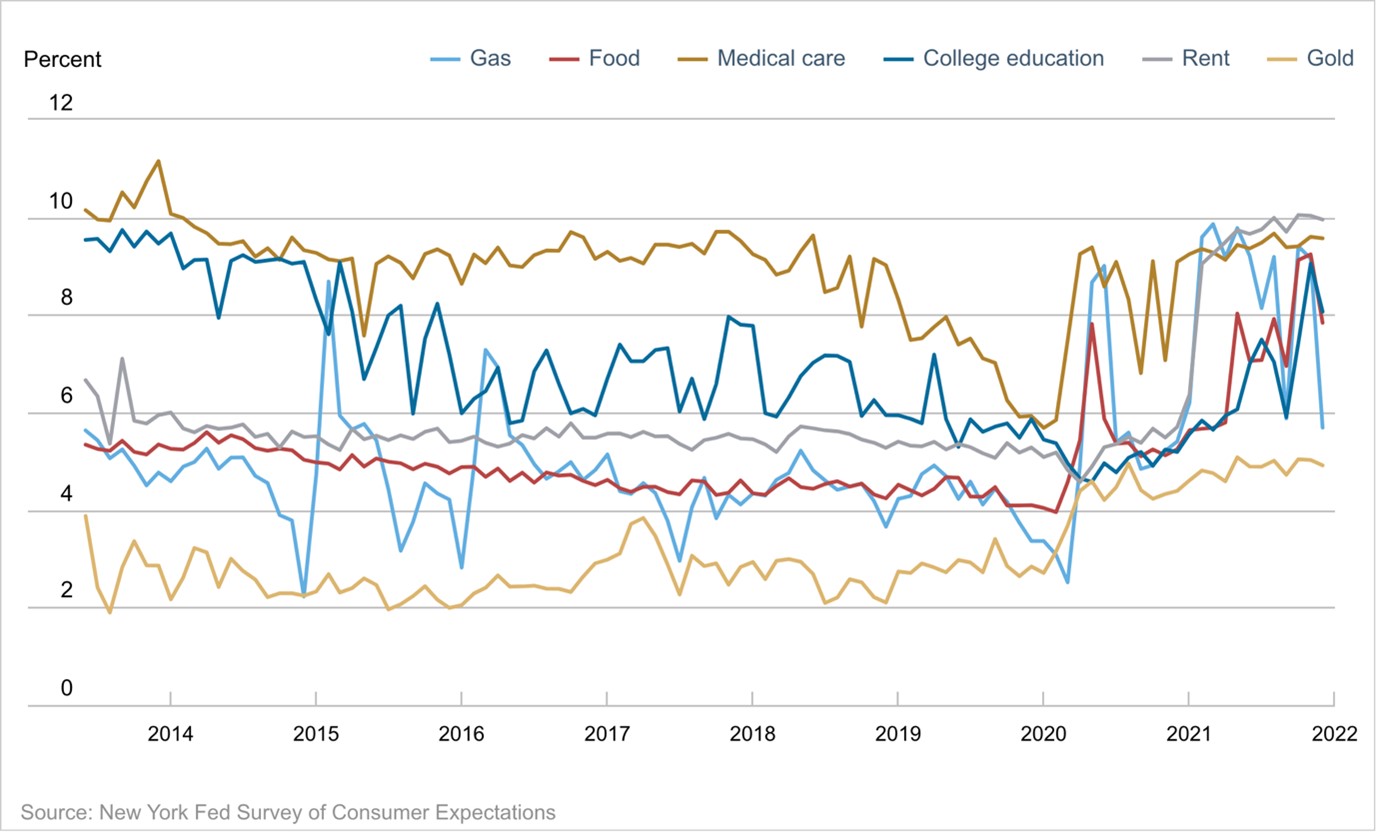

Both short and medium-term inflation expectations remain unchanged in the New York Fed’s December Survey of Consumer Expectations. Expectations are at record highs, especially for rent and health care. Both short- and medium-term horizons saw a decrease in uncertainty regarding future inflation. Though expectations for home price growth rose in December, they remained below their peak in May 2021. Households reported rising employment expectations, increased earnings growth, and reduced job losses. Income expectations are on the rise, so the next test will be whether households are going to be able to save or will have that earnings increase absorbed by higher costs of living.

{kind=link}