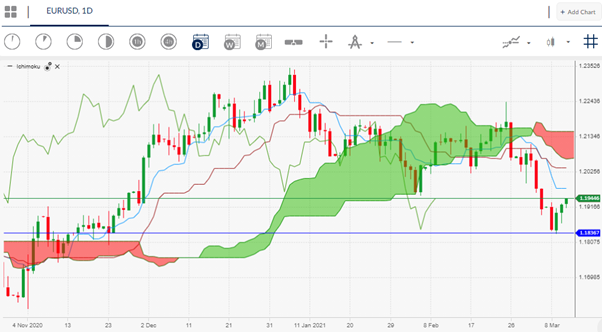

Today’s ECB meeting is expected to be another big event for the US dollar. With the EURUSD approaching the former yearly low, around 1.1950, the markets mood is finely balanced.

Sterling is also on the rise, and the British currency is likely to take its cue from whatever the euro does later today. The correlation between euro and British pound weakness has been breaking since the EURGBP broke under 0.8800 earlier this year, however, it could start to pick-up if the greenback continues last week’s down move.

Another interesting trade is the USDCAD. The Canadian dollar has strengthened since yesterday’s Bank of Canada meeting, and more so since the US dollar started bleeding lower in Asia.

{kind=link}