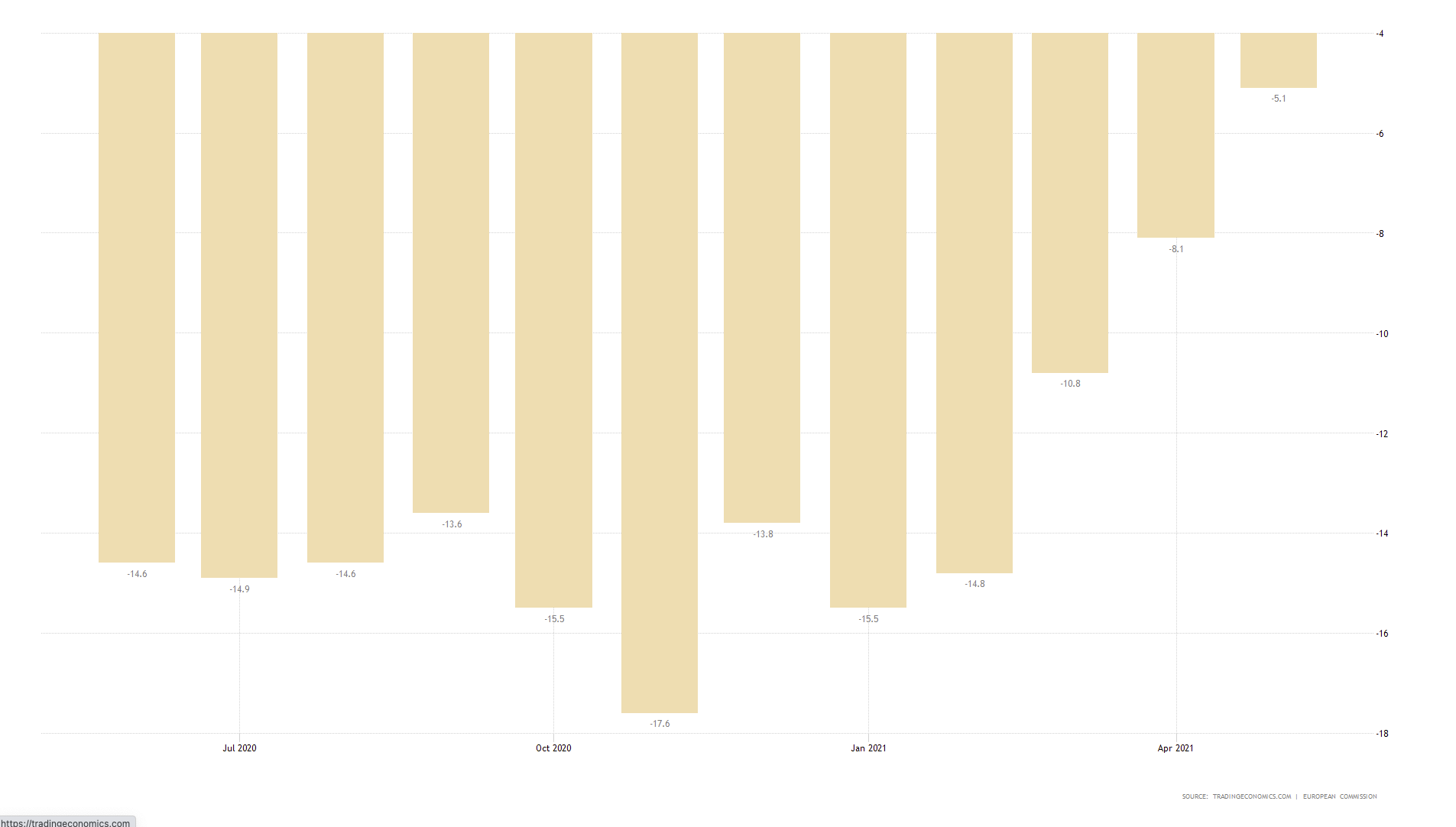

The EU consumer confidence Flash data for May, shows things are still pretty bad in the Eurozone, but getting slightly better. Today’s reading came in at -5.1 v’s the expected -6.8 and beats the previous reading of -8.1 for April.

Covid-19 variants are going to be a real problem for the world for a long time, and there is talk of having to be vaccinated yearly. Soon it will be as common to get a Covid jab as it is for the vulnerable to get a flu jab. Fingers crossed they can come up with a combo. The European Commission hosted a Global Health summit where the IMF proposed a $50B budget to beat the coronavirus, while the US VP Harris put a spanner in the works saying the USA were not prepared to sign an international treaty just yet, saying “I know some are eager to work toward a pandemic treaty. While we understand the intent, the United States believes that we need to first strengthen our foundations. Thankfully, we have opportunities to come together to do just that. Today’s summit, and the Rome Declaration, are opportunities. […] So let us work together,”. The USA is committed to strengthening its foundations first with the G7, G20 and WHO.

{kind=link}