The response to the better-than-expected ISM Manufacturing PMI by the US dollar was very bullish. If the close today is above the daily 9-period moving average, I will be considering a long US dollar trade for the foreseeable future as I felt the market had been prepping for a further down move today and will be now off-side. This would explain the large bullish candle we see at the time of the writing.

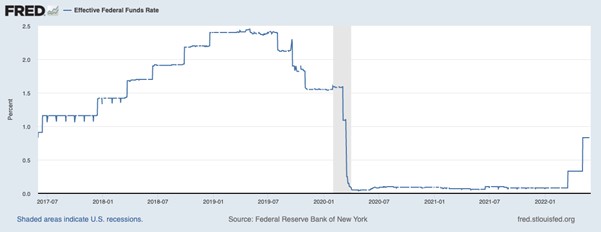

The Fed wants to destroy demand to bring inflation under control and also sees a tight jobs market as being a potential inflationary pressure too. Today’s Jolts job openings data in the United States decreased slightly in April compared to March, which will be seen as a positive to the Fed.

{kind=link}