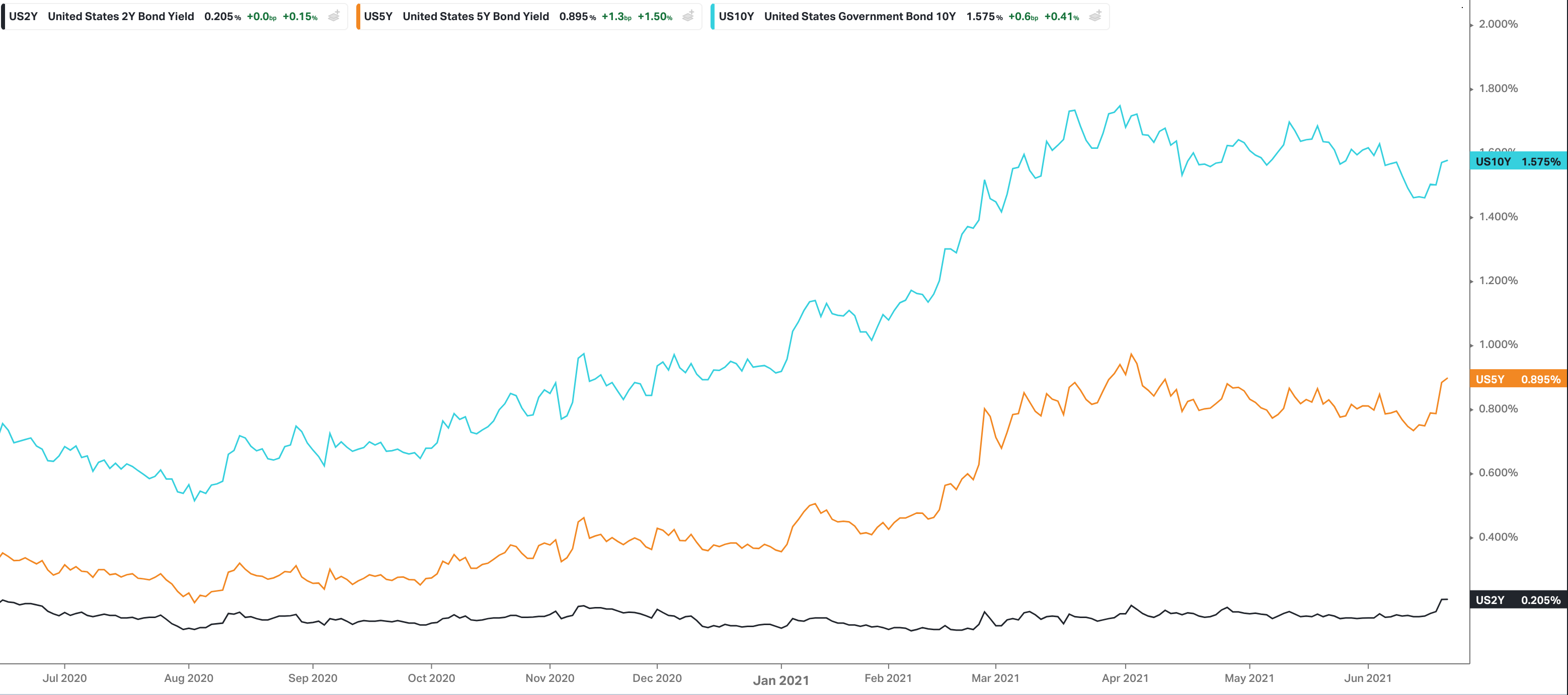

Benchmark bond yields rose on the release of the FOMC announcement, as did the US dollar index. But I am expecting yesterday’s move to be unwound in entirety as nothing has changed in policy and Chair Powell said explicitly to not take the dot plots and projections as gospel as no economists have any precedent to make accurate forecasts.

The FOMC have increased their inflation forecasts for the year. It now sees inflation running to 3.4% this year, above its previous estimate of 2.4%. The central bank also slightly hiked its PCE inflation estimates for 2022 and 2023. There were questions around transitory inflation affects as Lumber was mentioned as a case study of what can happen after a supply shock, increases costs on increasing demand, for the market to then rebalance and prices drop as demand disappears. The price of lumber will have to come back down to value before companies can buy with confidence and pass on the costs. Also, as supply came on stream timber merchants and building merchants will be awash with new supply and maybe excess. Again, forcing the prices of lumber further down.

When asked about the economic growth projections slowing down into the future, Chair Powell said that the committee would welcome a >3% GDP rate and that this year’s base effects will be distorting the current high levels of GDP and that over the course of the next couple of years increasing GDP figures are unlikely, but a growing economy is.

So how did the markets behave during all of this?

{kind=link}