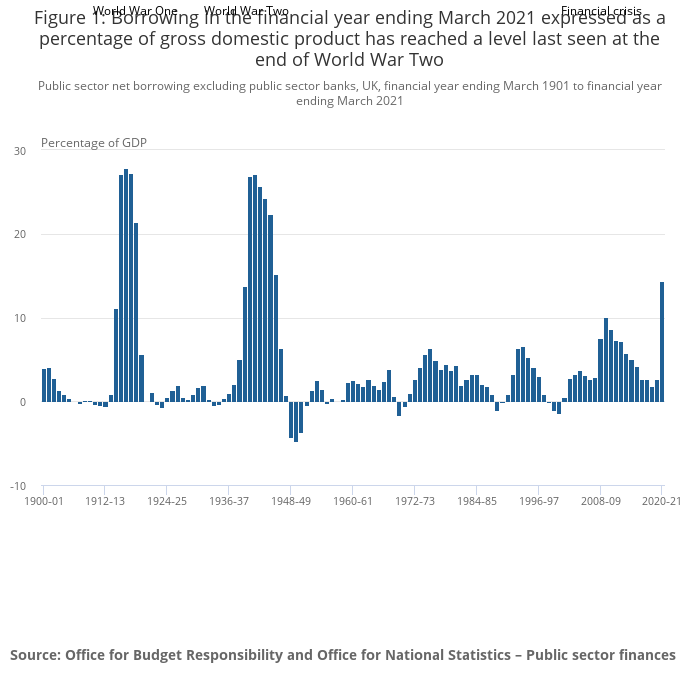

The UK has had to borrow due to the decrease in tax receipts from the disruptions caused by covid-19 lockdown measures. Public sector net borrowing (excluding public sector banks, PSNB ex) was estimated to have been £24.3 billion in May 2021; this was the second-highest May borrowing since monthly records began in 1993, £19.4 billion less than in May 2020.

{kind=link}