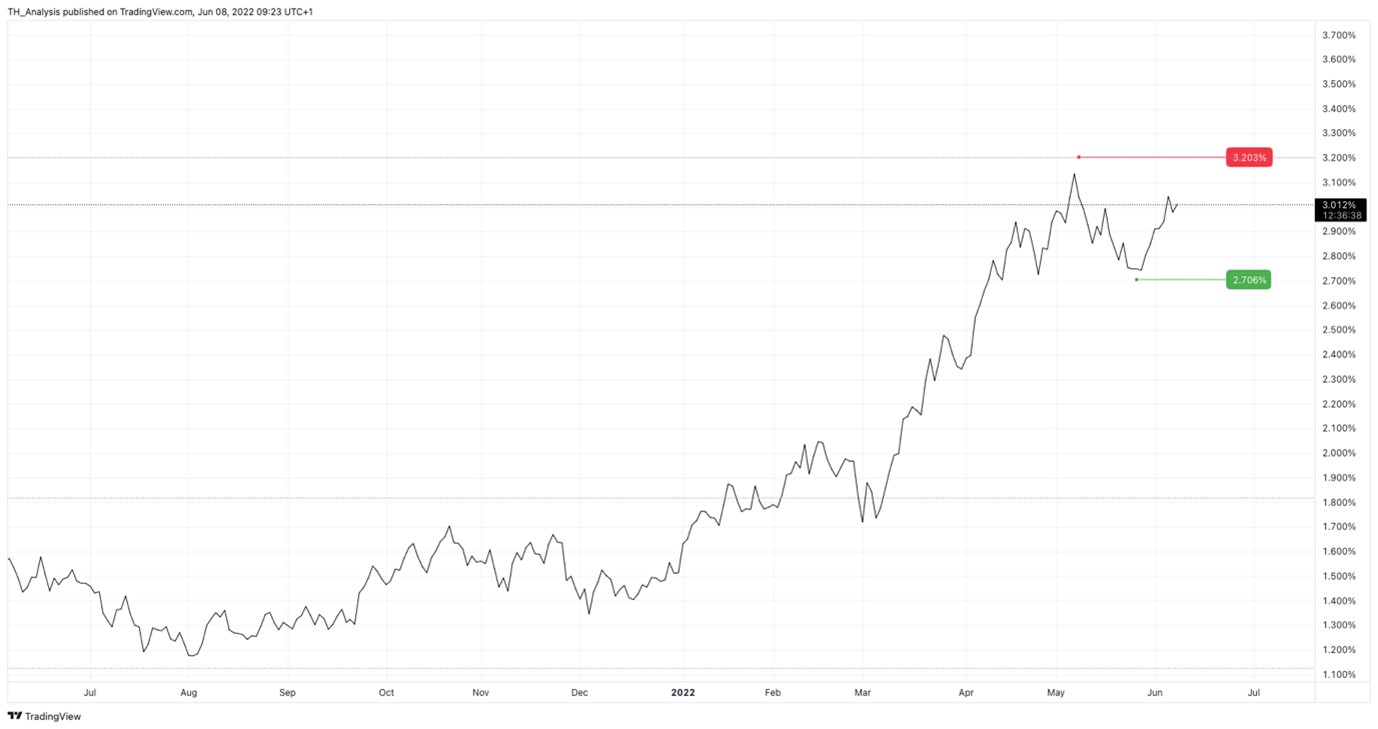

The US benchmark yield strength, combined with the higher prices in energy are keeping the USDJPY moving higher. There is a US 10-year Bond auction tonight and this has been a catalyst in the past for the US indices as they react to the fixed income markets. It could also be a turning point for the USDJPY. So something to lookout for.

The last two weeks in USDJPY has seen a basing around 126, and I have an upside target of 135.10 which is the January 2002 swing high. Being short the yen is the only trade that is really working out currently, so buying the dips in the GBPJPY, EURJPY or USDJPY is they occur is one strategy. The other is to wait for a consolidation and then take the breakout trade higher.

{kind=link}