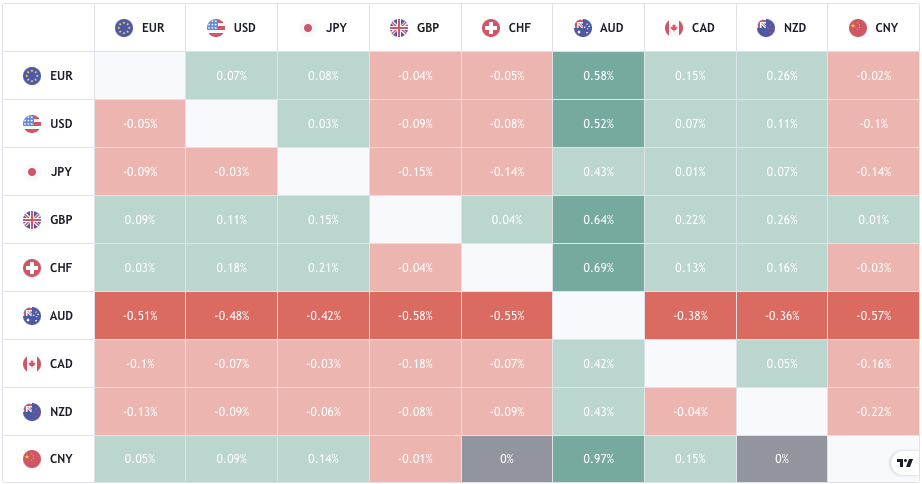

Again, for this currency pair to reach the significant swing highs and show a trend reversal, the DXY will need to drop. UK average earnings came in as expected and the unemployment rate is still above the pre-pandemic levels. Good news came in from the claimant count for unemployment change, which was down -58.6k showing a more resilient employment forecast.

The Japanese yen is under pressure after industrial production data showed a decrease of 1.5% month-on-month. The figure was in line with expectations with July’s index coming in at 100.4. On a monthly basis, the index of shipments and the inventories index both contracted by 0.6%, while the inventory rate grew by 1.2%.

Following on from hurricane Ida which caused an estimated $20-$30 billions worth of damage, the hurricane season continues with hurricane Nichols. The National Hurricane Centre (NHC) said on Tuesday that Hurricane Nicholas had made landfall along the Texan coast, with “heavy rain, high winds and dangerous surge ongoing.” The storm’s classification was officially upgraded to a Category 1 hurricane not long before landfall, with wind speeds of 75 mph.

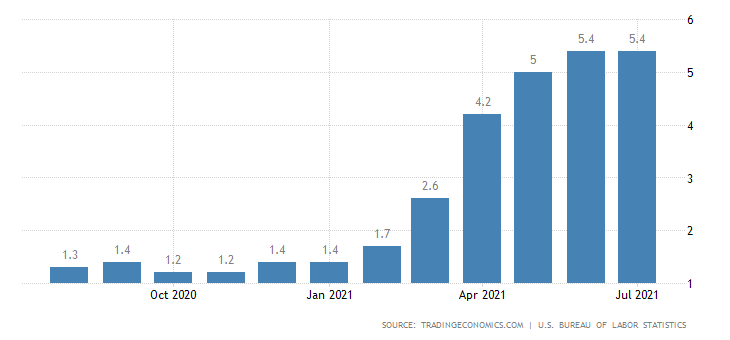

This afternoon the markets will be focusing on the US inflation data, with CPI month-on-month and core CPI likely to show inflation maintaining above target levels.

{kind=link}