Looking at a chart that compares the price of copper to the AUDUSD or (AUDJPY) and US10y02y yield curve shows how the Australian dollar tracks the inflation expectations and rising commodity prices.

Back in March 2020 the US 10y2y yield curve spiked higher, as the Federal Reserve and central banks globally put a floor in the markets with massive monetary stimulus. The expectations in the yield curve when it shows a steepening is a stronger economic activity and rising inflation expectations, and thus, higher interest rates. After that jump higher in the yield curve, the rise has been steadily moving along with the rise in copper price and the AUDJPY has matched the move quite tightly.

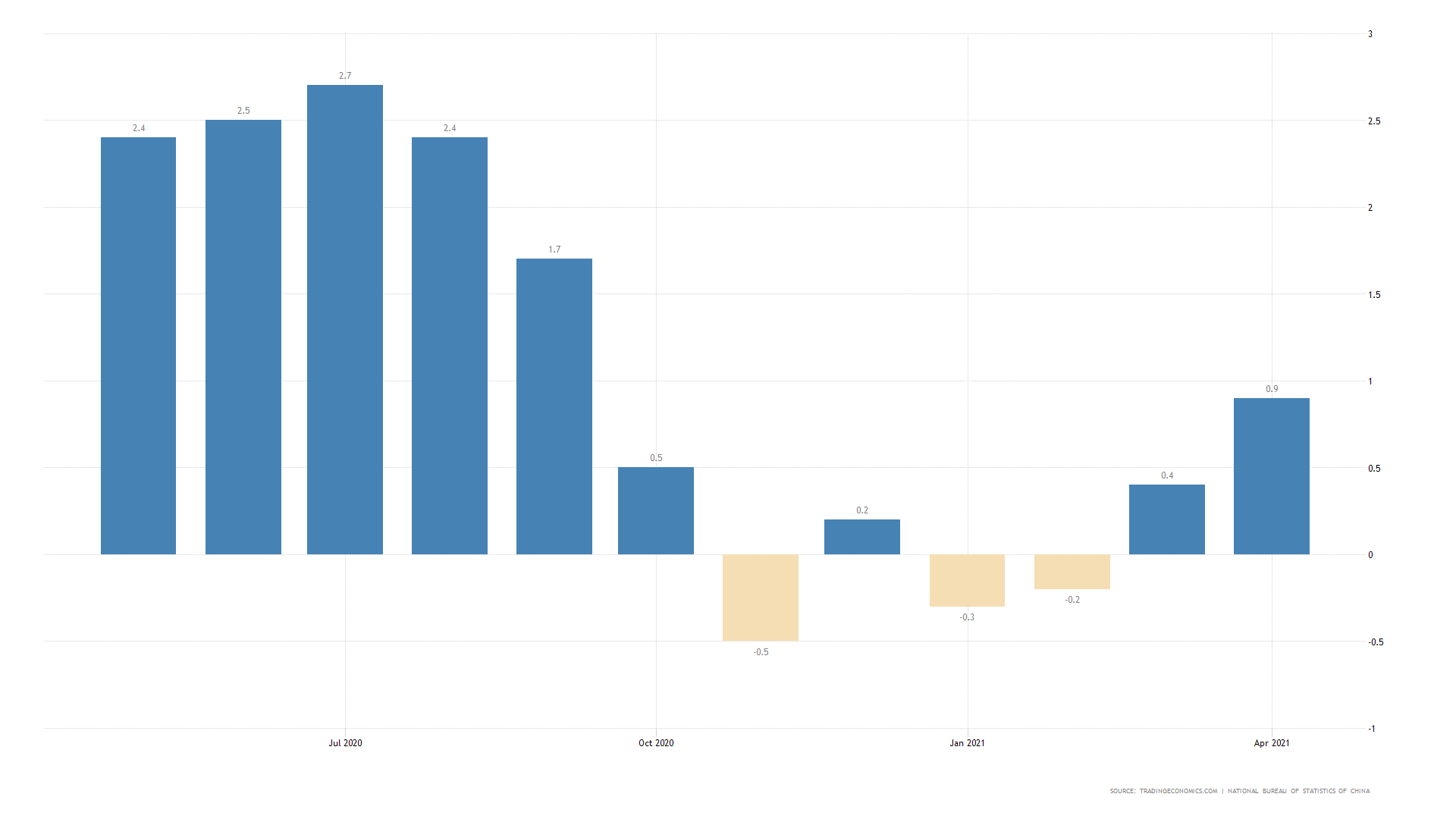

Over the course of the next few months, the Federal Reserve will want to see sustained inflation above 2%. If the CPI and PCE drop, the Federal Reserve will keep monetary policy loose, and the yield curve will likely adjust lower. This would bring the US dollar down and the AUDUSD should be saved from a major correction.

The risk is that while US inflation expectations are rising, the ongoing pandemic disruptions do not allow China to fully expand their economic activity and therefore creates uncertainty around sustained commodity demand. Plus, there are rising political challenges between the Australian and Chinese governments, which has resulted in a reduction of exports to China from Australia.

In the February Reserve Bank of Australia monetary policy statement, the RBA board stated “In the near term, some momentum in the global economy has been lost, as infection rates have surged in a number of economies and lockdown measures have again become necessary. The recovery is likely to be bumpy and uneven and dependent both on the health situation and ongoing fiscal and monetary policy support. Spare capacity will remain for some years, dampening inflationary pressures.”

Because of the uncertainties, the RBA are keeping their rate at 0.100%, so already well below the Feds 0.250%.

{kind=link}