The US dollar is gaining ground and should it get through these 200 daily exponentials moving average and market structural resistance the Swiss franc could depreciate rapidly.

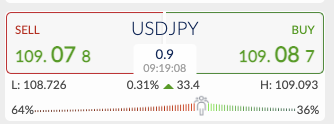

The bullish US dollar theme has meant that in the overnight session the Japanese Yen dropped to 108.980 bringing it down to 9-month lows. Emerging markets are becoming more vocal that higher US yields will lead to a financial crash in their markets, and one would expect a flight to safety in the yen would be the first course of action if the fed have to intervene and crush this rising Greenback.

{kind=link}