Português

Português Español

Español русский

русский

Commodity Analysis – Silver

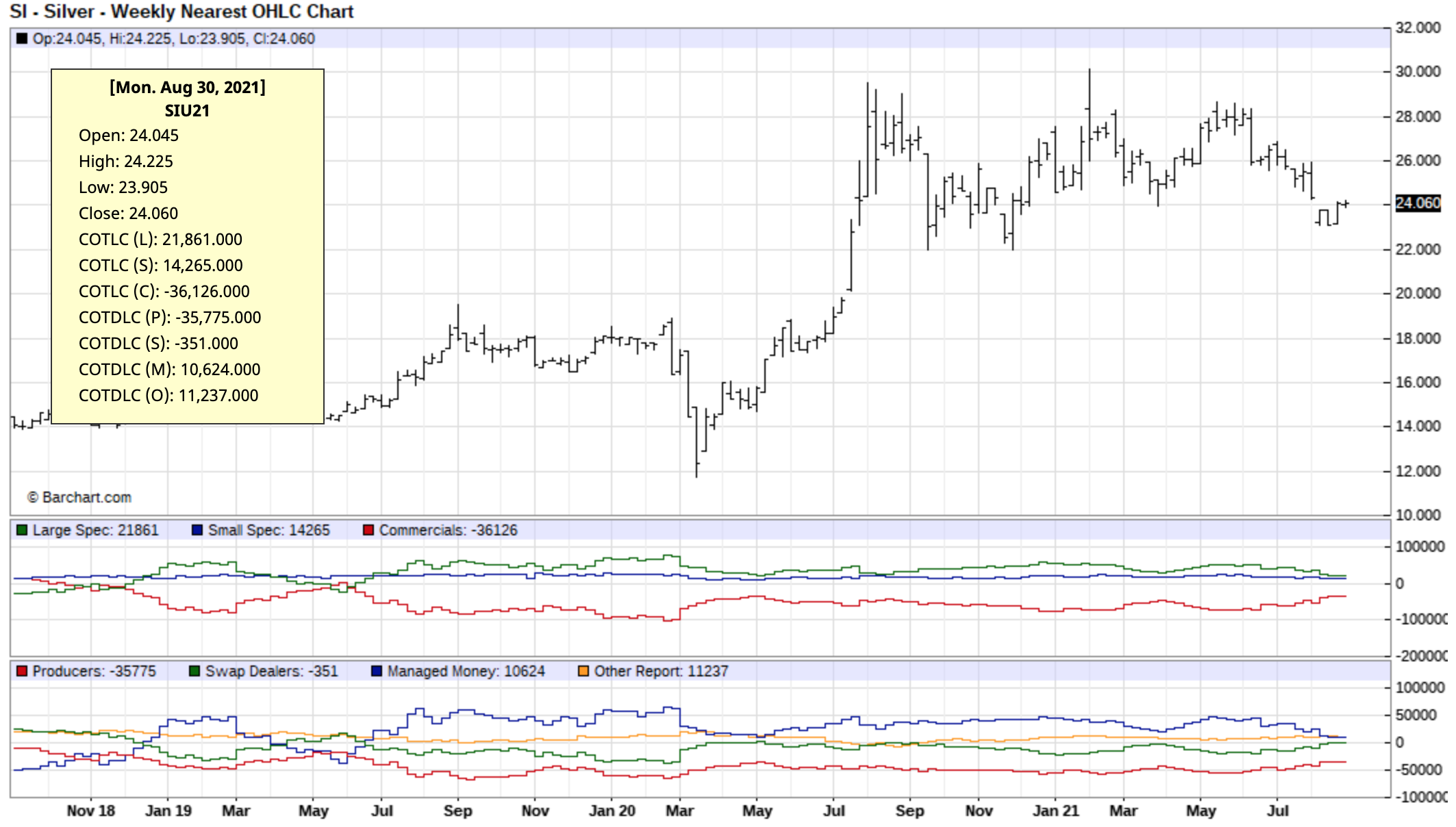

The markets can go up, down and sideways and currently the silver chart shows that the precious metal is in a sideways range between the $21.60 and $30 price levels. When a market goes into a corrective mode, it can be in price or through time and for the silver market it has mainly been across the x-axis rather than the y-axis of your charts.

In the mainstream media we often hear stories about manipulation, whether it be from the cohort of retail traders on Wall St. Bets pushing meme stocks, or their preferred broker (jokes) Robinhood who sell flow data to funds like Citadel. There was talk this year that the Reddit forums could be pushing the price of spot silver higher due to the well documented short paper interest and lack of physical supply. What hasn’t been mentioned in much detail across CNBC is what caused the precious metals markets to flash crash earlier this month at the start of trading on the 9th of August.

A few months earlier the media and market watchers had been talking up the impending Basel 3 regulations that were going to reclassify physical metals from a Tier-3 risky asset to a Tier 1 zero-risk asset that European banks could hold as part of their Net Stable Funding Ratio (NSFR).

NSFR’s wider objective, within the Capital Requirements Regulation (CRR) II framework, is to oblige banks to finance long-term assets with long-term money in order to avoid the liquidity failures seen during the 2007/08 global financial crisis. For precious metals, NSFR will require 85% of Required Stable Funding (RSF) to be held against the financing and the clearing and settlement of precious metals transactions.

Un-allocated or paper metal contracts would be deemed riskier assets and the banks would need to hold more reserves to keep them on the books within the regulatory guidelines. As stated above, the banks would need to hold 85% of the value of un-allocated contracts in zero-risk assets to back up the paper.

The London Bullion Market Association (LBMA) successfully negotiated out of having to be fully compliant but should be moving towards full compliance by the end of this year.

Because there are a lot of unallocated positions which make up the futures markets, it is reasonable to suspect that a co-ordinated effort to move prices lower was done during this holiday markets for some institutions to square their books as they move towards regulatory compliance. The effect was to instigate covering of unallocated by buying physical, but to buy physical you need someone to sell back to you.

During the flash crash early in August there would have been an opportunity for such an act as institutional traders could have Exchanged Futures for Physical which is known as EFP. – EFP is a backdoor for paper trades to get converted to physical contracts, where you can lock in a physical price through exchanging at a paper price.

Those traders that went into the weekend of the 7th of August long gold and un-hedged probably puked their position as the price dropped like a stone, and as prices accelerated lower, speculators would have opened up more shorts pushing prices even lower meaning you don’t need to use a lot of contracts to move the market in a major way, you just need to trigger a speculators algo that chases momentum.

All of this with the intention of buying the physical contracts in the liquidity event as institutions got the price they wanted through the EFP. The bids would have been placed at the price the weak hands of the physical (spot price) would have had the majority of their stops. The overall result would be those looking to get rid of unallocated contracts would have raided those with physical positions and made them sell the physical to them. A.K.A a switcheroo!

See real-time quotes provided by our partner.

What we now can deduct from this activity is that the lows seen at the beginning of August are more than likely the base level for everything to build upon until the end of the year. If this is true, the lows of 2020 are the inception of the current rally, the swing high from the beginning of 2021 is the anchor and the August flash crash low is the pull-back, which if you use in conjunction with a fib extension tool, the next levels for take profit are $40-$41/oz for the measured move then 161.8% extension comes in at $53/oz.

Even if the rally stalls at the first set of fib extensions that still brings in $31-$36/oz which is 3x the lows of 2020.

In the commitment of traders reports we are also seeing that commercial reporters are decreasing their short positions, which in March 2020 led to the start of the rise in silver from $12/oz to $30/oz. There are also mentions of refiners who make up part of the commercial reporting cohort, buying back deliverable silver contracts which are running at a discount to spot, to then redistribute to buyers and fulfil orders at a premium, because the physical market is so tight and there is a high demand.

US dollars has been in the safe haven flows as worries around the fed tightening were abundant since the Hawkish June FOMC. The silver to greenback ratio in safe haven flows have equalled each other out as prices have gone sideways in the XAGUSD but gold has had a lot of flows during these uncertain times.

With the uncertainty in the markets around transitory inflation, COVID-19 delta variant disruptions and the “will they, won’t they” raise rates from Fed watchers, gold is likely to receive safe haven flows as is the US dollar for longer. That has been the trend so far at least. When we know more about what the Fed are planning with monetary policy, we should eventually move to a US dollar bear trend resumption and the spot prices for silver and gold should once again rise.

See real-time quotes provided by our partner.

The US dollar index daily chart is showing that the 50-period exponential average and a previous swing low are currently acting as technical support. Watching for a break lower than today’s low price or better still below the daily 200 ema in blue, would be a good continuation trade for silver longs. Whilst the US dollar is receiving favourable flows to the long side, the silver traders should be waiting for the XAGUSD to come down to a support level to buy the dips.

Gold could be at $2300-$2500 on the Comex exchange as the likes of LBMA become physically backed by end of 2021 beginning of 2022 as per Basel 3 requirements. As the LBMA move from unallocated to allocated contracts the demand for physical will push prices higher. Two more delivery dates to keep an eye on are the October 2021 and December 2021 with the latter being a very busy month.

If the gold spot price were to rise, the 10-year trend for the Gold/Silver ratio could be 100:1 which would be silver remaining at current prices, but realistically 75:1 would have silver trading above $30/oz by the end of the year. Many silver investors believe the real (unmanipulated ratio) should be 16:1, which is why so many silver stackers get excited about the end of unallocated markets and rising precious metal prices. At a ratio of 16:1 and gold prices around $2300 by the end of the year, silver spot could be $143/oz which would be more than 10x the price in March 2020.

See real-time quotes provided by our partner.

$23/oz is a good line in the sand with every move down to that level being bought up in August. Obviously if we get above the current range highs for August and make a clear break, retest, and set up for a continuation higher that would also be bullish for the coming months. For now, my expectation is for this current channel to be tested a few more times before it is released and that will no doubt come with some market turmoil that puts most retail investors off. Keep an eye on the Sunday raids as these events can be good buying opportunities.

{kind=link}