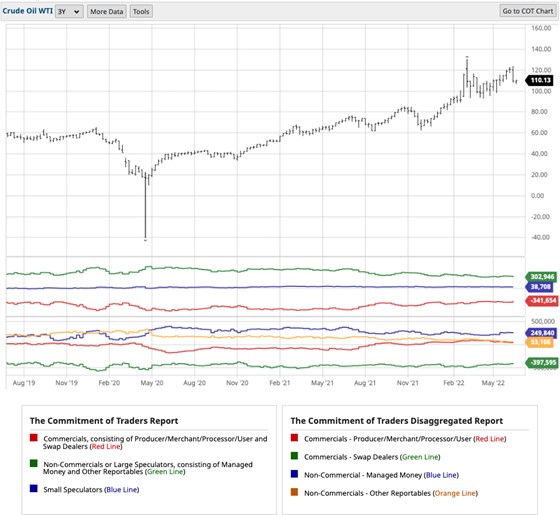

Today’s price action in Brent is at least $4 higher from yesterday’s low but what I am keen to see pan out today is whether the price action can break through and close above the low from the 16th of June at $113.72 per barrel. Looking left at the daily highs and lows, there are no other untested levels, so no resting orders left behind on the dip down. If we beak above todays current high and close near or above the daily 9-period EMA, I will take the lead from the COT report and be looking for a retest of the recent swing highs. There is also a chance that with the buying interest from the commercials in the latest dip feeding through it could lock in the $115 per barrel and price action could be sideways until we get the next major news from the likes of OPEC+. The ActivTrader sentiment indicator shows that the retail traders on the platform are positioned long with 57% of them expecting to see a test of $120 or above.

During the overnight session we learned more about the Reserve Bank of Australia’s thoughts on the Australian economy. In the RBA’s latest monetary policy meeting minutes, the committee acknowledged the recent increase in volatility in global commodity prices and agreed to take further steps to normalise monetary conditions in Australia over the months ahead. RBA Governor Lowe said that Australians should prepare for further interest rate hikes as the current level of rates is very low for an economy with a tight jobs market and high inflation. The RBA now expect the Australian CPI to top out around 7% in Q4 2022. But in 2023 inflation expectation dramatically drop back down to the 2%-3% range?

“The size and timing of future interest rate increases will continue to be guided by the incoming data and the Board’s assessment of the outlook for inflation and the labour market, including the risks to the outlook,” the bank stated. But while the cash rate is below 1% the monetary policy is still stimulatory. Further increases are required and at a rate of 25bps hikes at the next meetings the cash rate would be at or above 2.1% by year-end.

{kind=link}