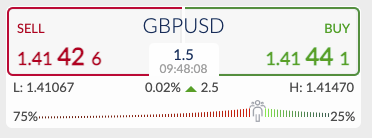

The AUDUSD is down today by 0.36% after forming a swing high structure this last few days.

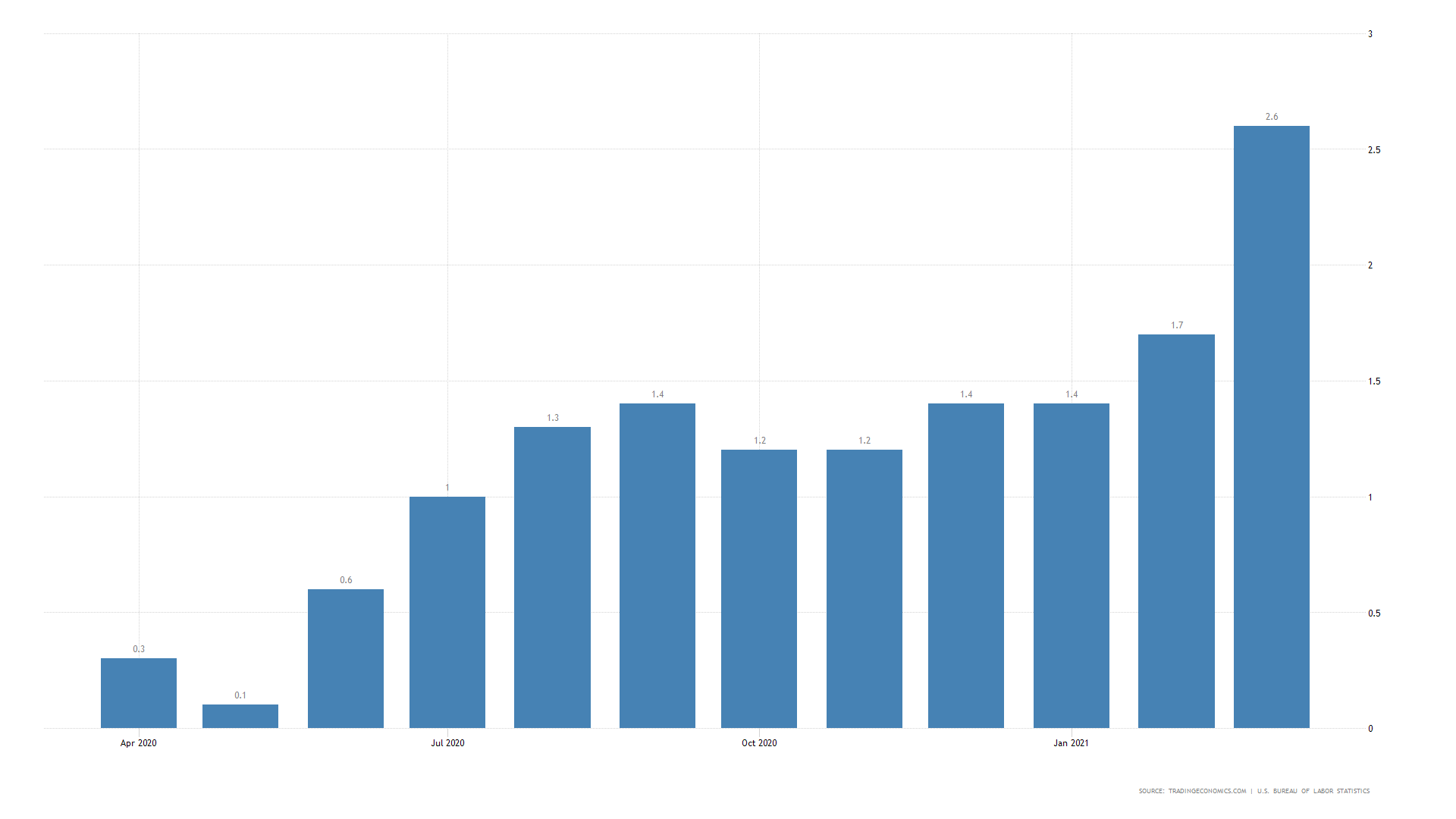

India’s COVID-19 statistics hit a new record high, in the past 24 hours, there were 4,205 coronavirus-related deaths, bringing the total number of coronavirus cases in India to 23,340,938. The hope for India is in the data showing recoveries from the virus now stands at 19,382,642, and more than 175 million doses of the coronavirus vaccine were administered in the country.

{kind=link}