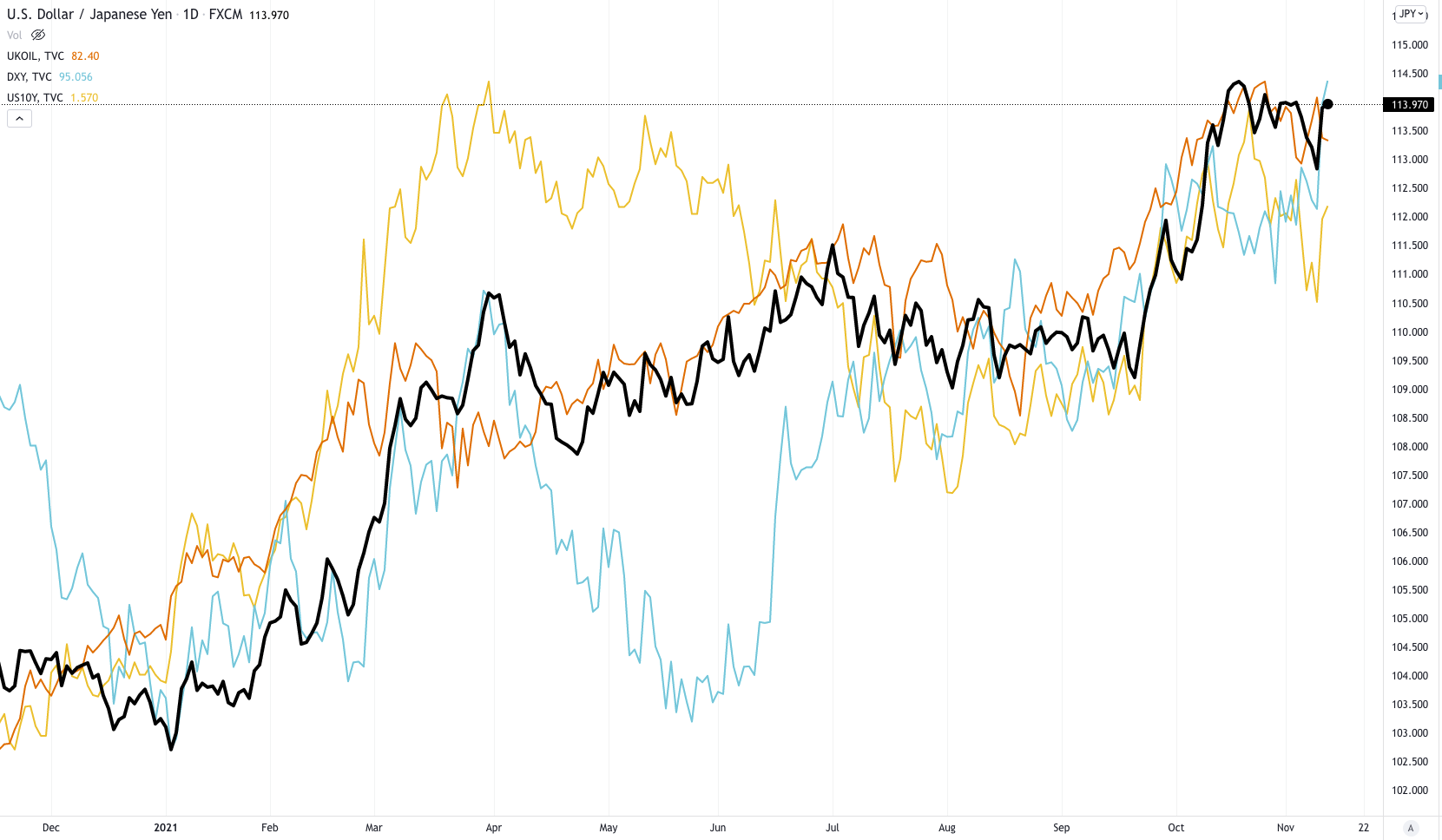

When price had reached the highs above 114.50, USDJPY had gotten significantly overbought as seen in the daily RSI indicator. I’m still looking for a breakout of the bull flag pattern to work out and when it does, ideally the daily RSI will still be under the key 70 level on the RSI. The recovery from the test of 113 in the last few days supports a buy on dips approach but with so much uncertainty around the US treasuries and the Fed rate hikes, I couldn’t buy the dip this time, as we could have been going lower to 111.50 under different circumstances.

In October, nonfarm payrolls showed a decent rebound in employment, although they remain 4.2 million below pre-pandemic levels. The 10 million JOLTS vacancies need to come down as the Fed are looking for participation to rise. Assuming the labour shortage due to rising COVID variants is behind us and people need to find work now that the enhanced benefits are ending, NFP should return to the 550k-600k range Fed Chair Powell talked of. If the labour markets show movement towards the maximum employment needed for rate hikes to commence, the US 10-year yields etc. will be leading higher and that has been good for the USDJPY.

{kind=link}