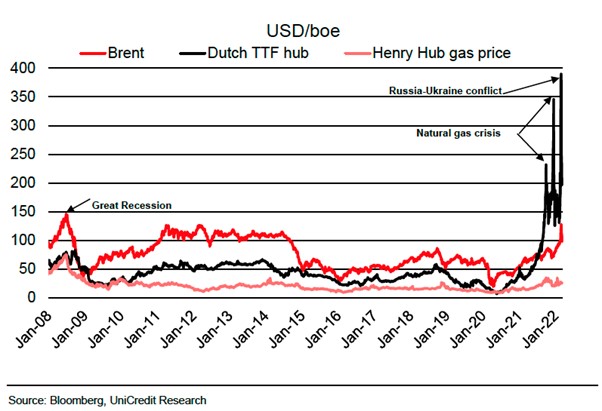

Vitol is a leading independent trader in crude oil and associated products with a global physical operation and they know a thing or two about the flows of energy worldwide. Their CEO today said that the company is observing some oil demand destruction and that the oil market will find it difficult to manage the disruptions to Russian oil. In his speech to the FT Commodities Global Summit, he made the point of saying that the gas markets were of greater concern than the oil markets. This was reiterated by the CEO of Gunvor, another global commodity trading house, who said the natural gas market is broken and in particular, the Dutch TTF.

From the summit we can ascertain that the markets are expecting a Russian oil production cut and with the added volatility in the markets it has become too expensive to hedge certain positions, so they are having to back away from the deals. The European Union has confessed to being too reliant on the Russians for energy but a transition away from this supply would take between 5 – 10 years. Of the reduction in Russian oil, exports may be totalling just over 2 million barrels per day, half of that could be replaced by Iranian oil if the nuclear deal could be signed off.

Investment bank Goldman Sachs has adjusted their Brent forecast for 2Q22 to $120 the 2H22 forecast unchanged at $135, based on a recovery in the Chinese demand assuming they get through these latest waves of covid disruptions. GS’s forecast for 2023 is for a modest drop to $110 on the basis that output will come from higher shale production in the US.

{kind=link}