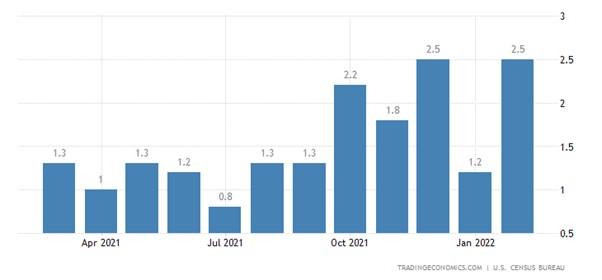

US loans and leases, as well as commercial and industrial loans, are higher this month than they have been since mid-2021. Lending has increased, and companies have restocked their inventories. In February, wholesale inventories increased by 2.5% compared with last month’s revised figure to $818.2 billion. Inventory levels for merchant wholesalers rose 19.9% compared to February 2021. The inventory to sales ratio for merchant wholesalers was 1.21, down from 1.27 a year ago.

With the cost of credit rising for the consumer, worries around persistent higher inflation and of course the cost of energy, consumers could start withdrawing and not be willing to accept these higher prices. What we need to keep an eye on to see whether these inventories can keep supporting the dollar is whether consumer sentiment reverses its downtrend, whether the factory and manufacturing data including new orders keeps growing and if the manufacturers can keep passing on the higher prices. With rising inventories companies are going to probably purchase less until inventories are depleted.

{kind=link}