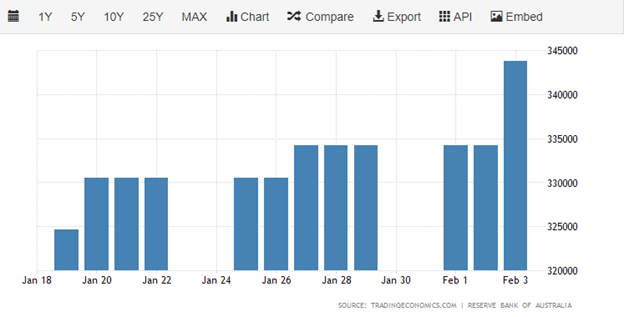

During the upcoming trading week, the release of central bank meeting minutes from the FOMC, Reserve Bank of Australia, and European Central Bank headline the economic docket. Market participants will be combing through the respective central bank minutes for clues about future central bank policy.

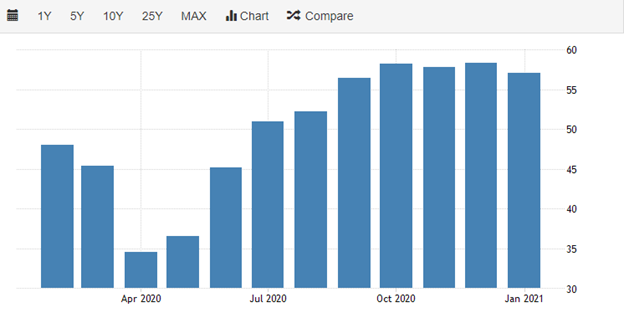

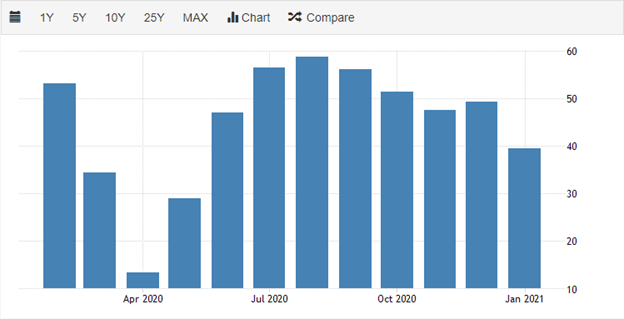

PMI manufacturing data from the eurozone, United Kingdom, and United States will also be another big focus for traders and investors. The global manufacturing sector has been a bright spot over recent months, particularly in America. Any signs of global PMI activity slowing could cause stock markets to turn lower.

Other highlights on the economic calendar include eurozone fourth-quarter GDP, ZEW data from Germany, and EU employment figures. The world’s second-largest economy, China, also releases important import and export data.

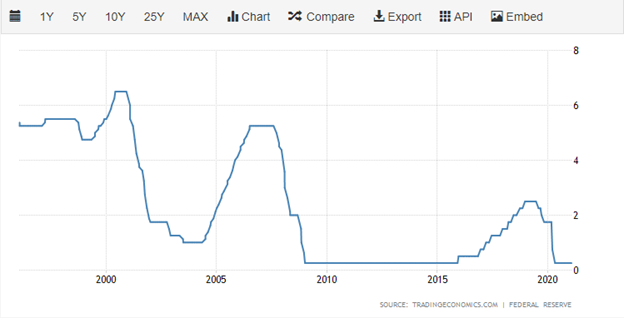

Central Bank Minutes

The FOMC meeting minutes this week is expected to relay to investors the central bank’s commitment to providing the US economy with adequate support during the ongoing COVID-19 pandemic.

Traders and investors are not expecting the FOMC to steer away from the dovish play book, especially given recent weak US jobs and inflation data. Overall, those seeking any hawkish commentary are bound to be disappointed.

{kind=link}